“Cash is king” has guided investors since the 1987 market crash.

But what if this so-called “king” is actually putting your retirement plan at risk?

Millions of retirees are lured by today’s enticing cash yields, confusing safety nets for sound investment strategies.

In this episode, I’m revealing why cash (even at 4-5%!) is a deceptive long-term investment.

I’m also sharing details about a critical investment performance metric to help you make more informed portfolio decisions.

If you’re wondering how to balance safety and growth in today’s uncertain market, this episode is for you.

Listen To This Episode On:

When You’re Ready, Here Are 3 Ways I Can Help You:

- Get Your FREE Retirement & Tax Analysis. Learn how to improve retirement success + lower taxes.

- Listen to the Stay Wealthy Retirement Show. An Apple Top 50 investing podcast.

- Join My Retirement Newsletter. Weekly retirement and investing tips (delivered to our inbox!)

+ Episode Charts

+ Episode Resources

+ Episode Transcript

You’ve heard that cash is king. But what if this so-called king is actually putting your retirement plan at risk?

This popular phrase was originally coined by the CEO of Volvo after the 1987 market crash, highlighting the advantage of having ample cash reserves during difficult times.

And just like Volvo back then, retirees often rely on cash reserves to protect themselves from financial storms.

However, many investors are mistakenly viewing cash as an attractive investment rather than a safety net, thanks to today’s 4-5% yields.

But beneath those attractive yields lies a hidden truth—a silent thief called inflation is slowly draining your wealth.

What feels safe today might cost you dearly tomorrow.

Welcome to another episode of the Stay Wealthy Retirement Show. I’m your host, Taylor Schulte, and every week I tackle the most important financial topics to help you “stay wealthy” in retirement. And now, onto today’s episode.

The Hidden Risk of “High-Yield” Cash in Retirement

Nominal vs. Real Returns

When evaluating investment performance, two primary metrics are often considered: nominal returns and real returns.

Nominal returns are straightforward—they’re the headline numbers you see before factoring in inflation, taxes, or fees.

For instance, if you invested $100,000 in the S&P 500 last year and now your investment is worth $110,000, your nominal rate of return is 10%. Nominal returns are easy to compare and widely cited; however, they don’t tell the full story.

The “real” rate of return (i.e., REAL return) reveals your true gains since it adjusts an investment’s nominal return for one important factor—inflation.

The real return is the percentage return of an investment after inflation is factored in. It’s an inflation-adjusted return.

And, yes, technically, the real return would also be net of things like fees and taxes, but I’m keeping it simple today and using a slightly simplified definition of real returns that just focuses on inflation.

Using the previous example of investing $100,000 in the S&P 500 one year ago…if the nominal return during that time period was 10% and inflation was 6%, an investor’s REAL RETURN was actually only 4%. Inflation – i.e., higher prices for goods and services – reduced the investor’s nominal return, and perhaps more importantly, their purchasing power.

With these definitions in mind, nominal returns will, of course, always be higher than real returns, except when inflation is absent or we are experiencing deflation.

But in a normal environment, some level of inflation exists. Historically, on average for the last 95 years, inflation has hovered around 3%. So if you earn 10% on an investment, nearly ⅓ of that NOMINAL return gets eaten up by inflation, sometimes more, sometimes less.

Because yields and returns are often quoted in nominal returns, real returns are often overlooked by investors. For example, I regularly hear retirement savers talk about the early 1980s and the double-digit yields they were earning on cash and bonds…but then fail to reference the rate of inflation during that time period…or the double-digit interest rate they were paying on their mortgage.

Psychologically, it just feels better to us to earn a healthy rate of return on our cash, even if our inflation-adjusted return is, more or less, in line with historical averages. Especially coming out of a period where cash yields were nearly 0% for what felt like an eternity.

The Risk of Today’s High Cash Yields

Today, money markets and CDs yielding upwards of 5% appear attractive, especially after years of near-zero returns. Yet, this perception misses a crucial point.

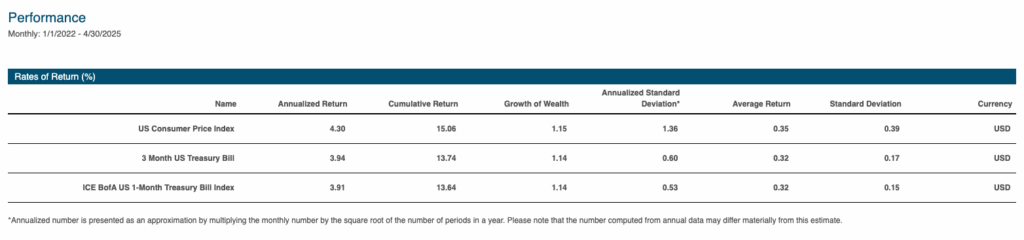

For example, from January 1st, 2022, to April 30th, 2025, Vanguard’s Treasury Money Market Fund (VUSXX) returned about 14%, averaging nearly 4% per year. However, inflation during this same time period eroded every bit of that return and a little more, leaving money market investors with a negative 1.42% REAL return. And that doesn’t even include taxes!

So, for the last 3 years since yields started to rise, investors might have felt like they were finally getting paid an attractive return to invest in risk-free money markets, CDs, or treasury bills. But, in reality, they were missing out on superior stock market returns, losing money to inflation, and earning a negative real return.

Surprisingly, this cash environment isn’t very different than the frustrating time period from 2009 to 2020 when the average money market return was only about 0.4%, and inflation averaged around 1.6%. Cash yields were well below historical levels, but so was inflation, leaving money market investors with negative real returns, once again.

And, yes, I am cherry picking a few recent time periods here to help make the point that nominal returns don’t tell the whole story. It’s worth noting that from 1978 to 1999, cash did outpace inflation by about 3% per year, on average. But that is one single unique time period and likely shouldn’t be expected or used as a planning assumption.

It’s also worth noting that, during that 21-year span from 1978 to 1999, US stocks outpaced inflation by about 12% per year, on average. So, even though risk-free cash had a positive real return, it was a fraction of what the equity market delivered during that time period.

As always, longer time frames are more prudent to evaluate and help investors set better expectations with their investments and planning.

For the last 97 years, one-month treasury bills (a good proxy for cash and money markets) returned about 3% per year, on average. You likely won’t be surprised to learn that the average rate of inflation during that same time period was roughly the same. In other words, over long periods of time, investors should not expect money, markets, CDs, or treasury bills to outpace inflation and increase their purchasing power.

And this highlights exactly why smart retirement investors allocate a healthy percentage of their nest egg to riskier asset classes—to earn a positive REAL return and protect their purchasing power.

So, while I believe investors should be smart with their cash management and ensure they are earning a competitive return on the money they need to keep safe, I don’t think we should view today’s 4-5% cash-yielding environment much differently than in years past. Sure, we might get lucky and catch a short period of time where money markets outperform inflation or even stocks and bonds, but that isn’t a reasonable long-term expectation.

Investing is a risk/reward decision. If we want to earn healthy and positive REAL returns that allow us to reach our retirement goals and/or enjoy spending money in retirement without putting our plan in jeopardy, we have to accept a certain level of risk.

We also have to be careful viewing cash as a long-term investment. In the accumulation phase of life, investing a large % of savings in cash is a sure way to reduce both nominal and real returns.

Go back to that time period from 1978-1999 that I referenced earlier when cash had some of the best real returns in history. Sure, you outpaced inflation by about 3% per year during those 21 years, but the US stock market turned $100,000 into $3.3MM during that same time period. That was a significant wealth-building opportunity that most long-term savers couldn’t afford to miss.

On the other end of the spectrum, those who are in retirement viewing current money market and CD yields as a smart, low-risk investment are increasing the chances of inflation eating away at their purchasing power.

In a worst-case scenario, inflation can swallow up their entire nest egg. For most retirees, a positive REAL return–a return above and beyond the inflation rate—is required in order to maintain spending from a portfolio over a 30+ year retirement. And, in order to achieve that, an investor needs to allocate some portion of their portfolio to riskier, higher-returning investments.

Cash is Not a Bond Alternative

Before I wrap up, one response I often hear from retirement investors is that investing in cash right now is a bond replacement for them. They don’t think bonds are a good investment, and they would prefer to invest in money markets or CDs. The challenge with this approach, however, is that money markets and CDs don’t produce the returns that a retirement investor might need when a catastrophic event occurs.

For example, rewind back to the Great Financial Crisis. From October 2007 to the bottom of the market in March of 2009, the US stock market was down over 50%. While money markets had a total return of about 3% during that same period and provided stability to investors, US intermediate treasury bonds returned over 16%.

That 16% return during the second-worst recession in history was wildly helpful to a retiree taking regular withdrawals from their portfolio to fund their retirement. They would have been able to withdraw money from the appreciation in their bonds (or as we call it, their war chest) while their stocks went on a wild ride for 18 months.

Again, this shouldn’t necessarily be surprising. Intermediate treasury bonds contain more risk than money market funds or short-term T-bills. If you take more risk with your investments, you should expect a higher rate of return.

To avoid any confusion, this is not an either-or decision. Retirement investors should have a mix of cash, short-term bonds, and intermediate-term bonds to round out and fill up what we call their war chest. A simple rule of thumb is to establish a war chest of cash and bonds that equals 2-5 years of living expenses. It might equal 2 years if you want or need to take more risk, and it might be closer to 5 years if you are ultra risk-averse (or your plan doesn’t require more risk because you have oversaved for retirement).

Cash is king. And for those who are in retirement or close to it, a healthy cash balance is absolutely needed to weather unpredictable storms, as the Volvo CEO famously stated. But cash is not a long-term investment. Higher yields might seem attractive until we factor in fees, taxes, and most notably, inflation.

Equally as important, higher cash yields should not lure long-term retirement investors into thinking that they can outsmart the markets and achieve a higher return with less risk. Risk and return go hand in hand. If we want to have a successful retirement plan…if we want to maximize our retirement income while mitigating the chances of running out of money throughout a 30+ year retirement, we have to make 30-year investing decisions. Chasing short-term trends, even with an asset class as boring as cash, will only increase the long-term risk of our plan.

Once again, to view the research and articles supporting today’s episode, just head over to youstaywealthy.com/243.

Disclaimer

This podcast is for informational and entertainment purposes only, and should not be relied upon as a basis for investment decisions. This podcast is not engaged in rendering legal, financial, or other professional services.