Today I’m talking about the current banking crisis.

Why?

Silicon Valley Bank (SVB) and Signature Bank were the 2nd and 3rd largest bank failures in history, respectively.

In addition to explaining how we got here and why these banks collapsed…

…I’m answering three (3) important questions that retirement investors are asking.

Key Takeaways

- Is this a repeat of 2008/2009?

- Is your money safe? Should you be worried that your bank is next?

- What about cash in your investment accounts? Is that protected?

If you’re ready to understand what this banking debacle means and what to do in response, today’s episode is for you.

Need Tax + Retirement Planning Help?

We specialize in helping people aged 50+ lower taxes, invest smarter, and (safely) create a retirement paycheck.

Our Free Retirement Assessment™ will answer your BIG questions and help you properly evaluate our firm.

Click the banner below to learn more. 👇

Listen To This Episode On:

When You’re Ready, Here Are 3 Ways I Can Help You:

- Schedule a Free Retirement Strategy Session. Get your questions answered + learn how we can help you improve retirement success and lower taxes.

- Listen to the Stay Wealthy Retirement Show. An Apple Top 50 investing podcast.

- Join My Retirement Newsletter. Weekly retirement and investing tips (delivered to our inbox!)

+ Episode Resources

- Subscribe to the Stay Wealthy Newsletter! 📬

- Where $5 Trillion in Government Stimulus Money Went [NYT]

- Largest Bank Failures in History [Visual Capitalists]

- SVB is Bankrupt: What Really Happened [Cullen Roche]

- Two Worlds [Morgan Housel]

- Fidelity Treasury Money Market Fund [FZFXX]

- Fed Funds History [Forbes]

- MaxMyInterest:

+ Episode Transcript

Silicon Valley Bank was the 16th largest bank in the country.

And, two weeks ago, on March 17th, they filed for bankruptcy.

It was the second biggest bank failure in US history behind Washington Mutual.

Signature Bank, headquartered in New York, collapsed shortly after and became the third-largest bank failure on record.

What exactly happened? Why did these banks fail? Whose fault is it? What can retirement savers learn from this debacle and what should they do in response?

Welcome to the Stay Wealthy podcast, I’m your host Taylor Schulte, and today tackling these questions in addition to answering 5 important questions about our banking system.

For the links and resources mentioned, head over to youstaywealthy.com/184.

The Banking Crisis: 3 Things Retirement Investors Need to Know

To understand what happened with Silicon Valley Bank and the current state of the banking system, we have to rewind a few years.

In early 2020, the growing instability surrounding COVID-19 caused the global markets to collapse.

In just four short weeks, the U.S. stock market dropped 34%.

By April, the unemployment rate was skyrocketing and hit a high of 14.7%.

And by the end of June, real GDP, i.e., the output US economy, was cut by a ⅓.

In response, to prevent things from getting worse, the government stepped in, and congress-approved stimulus bills unleashed the largest flood of federal money into the U.S. economy in history.

When it was all said and done, approximately $5 trillion went to American households, small businesses, restaurants, airlines, hospitals, local governments, schools, and other institutions around the country.

According to Louise Sheiner, an economist with the Brookings Institution, the stimulus

“made sure that when we reopened, people had money to spend, their credit rating wasn’t ruined, they weren’t evicted and kids weren’t going hungry.”

In addition to flooding the economy with money, the Federal Reserve cut interest rates twice, taking already historically low-interest rates even lower.

The Fed also began Quantitative Easing again and established new lending programs, including forgivable loans to businesses.

2020 ended up being the best year for household income in American history.

In addition, total monthly debt payments as a share of income were the lowest in history and consumers had $1 Trillion more in checking accounts than one year prior.

In other words, financially speaking, Americans were in a wildly better position at the end of 2020 than at the end of 2019.

Now, with interest rates at record low levels, consumers are incentivized to take their excess income and savings and spend it and/or invest it.

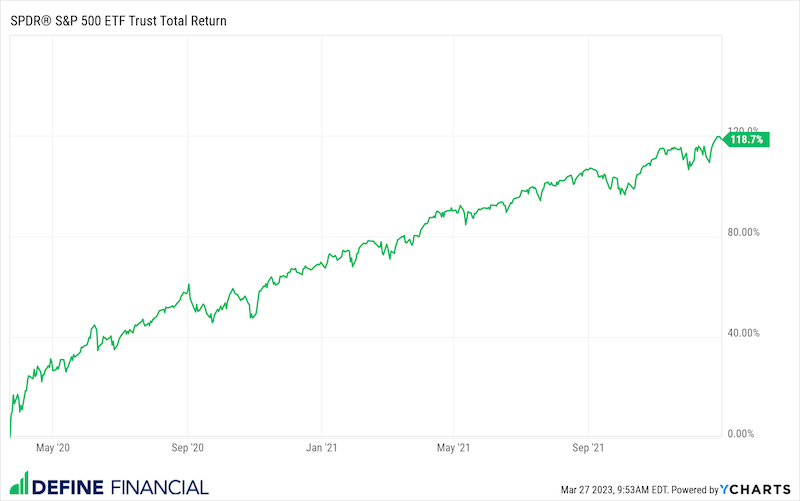

As a result, from March 23rd, 2020 to December 31, 2021, the S&P 500 was up about 120% as people piled money into the markets with renewed confidence in the economy.

And this is where this chain of very unique events begins to collide with banks like Silicon Valley Bank.

Similar to consumers, Venture Capitalists were also incentivized to allocate their excess cash given record low-interest rates. As a result, they invested hundreds of billions of dollars in tech startups. In many cases, tech startups that weren’t even profitable.

In turn, those tech startups deposited their newly received venture capital money with banks like Silicon Valley Bank. In fact, Silicon Valley Bank’s deposits tripled from $60 billion in early 2020 to $200 billion in early 2022. And just like many banks, Silicon Valley Bank took those deposits and bought safe U.S. Treasuries, the most secure assets on the planet.

So, what’s the problem?

Well, while all of this was going on, inflation was growing in the background, hitting 9.1% in June of 2022, the highest level we’d seen since the early ’80s.

To combat inflation, the Fed determined they needed to slow down the economy. Consumer demand for goods and services far exceeded supply. So, to slow down the economy, they began raising interest rates. By the end of 2022, the Fed had raised rates 7 times.

As I’ve talked about before here on the show, while the fed doesn’t control bond yields, it can influence them. And bond yields were certainly influenced, we saw two-year treasury bond yields go from basically paying nothing to almost 5% in 18 months.

And, as we all know, when bond yields rise, bonds fall in value. Even AAA-rated extra safe treasury bonds…like the bonds that Silicon Valley Bank had purchased.

So now the economy begins to slow down due to the fed’s actions. And with a slowing economy, those profitless tech startups need some of their money they had piled into checking accounts.

In order to fulfill these withdrawal requests, Silicon Valley Bank had to sell some of their treasury bonds they had previously purchased. But, as we now know, those investments were in the red due to the rapid spike in yields. So they’re forced to sell investments at a loss – initially a 2 billion dollar loss – to meet the increasing number of withdrawal requests.

And as venture capitalists began to put two and two together, recognizing the situation Silicon Valley Bank was in, they begin urging their tech startups to get their money out ASAP. In a single day, $40 billion was withdrawn.

In other words, there was a run on the bank, ultimately rendering them insolvent, leaving them no choice but to file chapter 11.

This, naturally spooked customers at other banks around the country, leading them to start withdrawing cash before their banks followed suit.

What we’re seeing play out right now is what finance and economic nerds call your traditional credit cycle.

The cycle begins with economic expansion, followed by an uptick in inflation.

Then, as we’ve seen recently, the fed steps in and hikes rates to slow the economy down.

Consumers, as a result, start to borrow more money to make up for lost income in this, newer slower economy.

In turn, lending standards tighten, the economy contracts, and to complete the cycle, the Fed comes back and cuts rates to avoid a prolonged economic downturn.

As you have likely picked up on, with regard to the two bank failures, it’s hard to point the finger and assign blame to any one person or thing. From covid to the fed to congress approved stimulus bills to inflation to venture capital firms to tech startups to banks receiving hundreds of billions of dollars in new deposits.

I’m not trying to let anyone off the hook here, but we’re staring at a very unique chain of events, a unique chain of events that may take years or even decades to fully understand the long-term impact.

So, instead of debating the nuances and trying to read between the lines of recent actions and commentary, I want to use the rest of our time today to answer 3 important questions about the current banking situation – 3 common questions that I’ve been asked recently that relate directly to retirement investors.

Question 1 – Is this a repeat of 2008/2009?

While I did mention Washington Mutual at the top of the show today, and shared that these two recent bank failures are the 2nd and 3rd largest in history, the current situation, and the current state of the banking system, is much different than what we witnessed in 08/09.

In addition to tighter lending standards, bank reserve requirements are much higher today than in the early 2000s.

In other words, banks are required to hold onto a much larger amount of money that can’t be used for things like lending out to other people. The reserve is intended to ensure that the bank can meet its liabilities in the case of sudden withdrawals.

In addition to higher reserve requirements, banks today are buying safe government bonds with some of those reserves, whereas in 08/09 banks were buying tranches of low-grade bonds that ultimately defaulted.

So, the problem with Silicon Valley Bank wasn’t that they financially unhealthy or that they made risky bets with their assets. The problem was their business was highly concentrated in one sector, the tech and startup sector. This concentration, coupled with the bank’s mismanagement of interest rate and liquidity risk, ultimately led to the collapse. Rapidly rising interest rates, and the series of events we reviewed today, certainly fueled the fire, but plenty of other banks around the country are holding up just fine.

So, no, it doesn’t appear to be a repeat of the great financial crisis. But we’re not totally out of the woods yet and may see some new, similar events play out in the coming weeks and months. But, thankfully, banks are in a much healthier position today than they were 15 years ago.

Which leads nicely into question two – Is your money safe? Should you be worried that your bank is next?

First, it’s worth noting that not a single bank customer has lost their money in an FDIC insured bank since 1933, including money that was above FDIC limits. And so far, no depositors appear to be losing any money this time around either. Last week, the Fed stated, “No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.”

However, the Fed also went on to state:

“Bank shareholders and certain unsecured debtholders will not be protected. Senior management has also been removed. Any losses to the deposit insurance fund to support uninsured depositors will be recorded by a special assessment on banks, as required by law.”

In short, the fed is not interested in protecting the bank’s bad actors or shareholders but is adamant about protecting consumer deposits, even deposits that exceed FDIC limits. And they’re largely doing this to maintain consumer trust in banks around the country to prevent this situation from escalating. The last thing we need is everyone racing to their local bank to pull everything out and stuff it under the mattress.

To be extra clear here, if you bank with an FDIC insured bank, you’re insured for up to $250,000 per individual. So, if it’s a joint account with you and your spouse, your cash deposits in a checking account are insured for up to $500,000. Your small local FDIC insured bank could go out of business tomorrow, and the deposit insurance fund would make you whole.

And while the fed is insuring dollars above and beyond the current limits at Silicon Valley Bank and Signature Bank, it’s not worth rolling the dice on what they do the next time this happens, and these recent events serve as a good reminder to keep your cash under the limits.

If needed, hold cash at multiple banks or use a service like MaxMyInterest who we’ve had on the show before to help keep your cash fully insured. You can also consider bank alternatives, like treasury backed money market funds.

Which takes us to question #3 – What about cash in your investment accounts? Is that cash safe from the current banking debacle?

The first thing to know is that some brokerage firms do have a banking arm, and as a result, cash inside an investment account can, by default, be held in a bank deposit fund similar to that of a bank. So, if your brokerage firm is maintaining your cash in a bank deposit fund, you would want to keep your cash balance under FDIC limits.

You would also want to talk to your brokerage firm or advisor about alternatives, such as US treasury money market funds. Instead of the FDIC protecting your cash, it’s the full faith and credit of the US government. In short, unless the US government goes out of business, your cash is safe.

And for that reason, there is no limit to the amount of cash you can hold…some investors will hold tens or even hundreds of millions of dollars U.S. government money market funds.

For what it’s worth, the fund we use for our clients is the Fidelity Treasury Money Market Fund FZFXX which currently has a yield of just over 4%. For clients with over $1mil of cash, we gain access to FSIXX, which has lower costs, and boosts the yield by about 20bps. Most brokerage firms have something similar, just take note of the underlying fees as they will directly reduce the yield.

Lastly, just to be sure we cover our bases here and prevent any confusion, if you have money invested in stocks, bonds, ETFs, mutual funds, etc. they are not impacted by any of the banking concepts we discussed today.

For example, if you own XYZ mutual fund at Charles Schwab, and Charles Schwab goes out of business tomorrow, you still own your shares of XYZ mutual fund. Same can be said for other publicly traded securities. You have ownership in those companies, or the underlying companies owned by the mutual fund, and not the brokerage firm that maintains custody of your investments.

I know today’s topic was complex and wide-ranging and there are many more pieces to the puzzle that I didn’t get to. But I hope you found it helpful and brought some clarity to a unique situation. If anything, I hope it served as a good wake-up call that cash management is important, and while most Americans don’t have cash above and beyond FDIC limits, it’s important to know where our cash is held, how we’re protected, and what we can do to optimize that asset class.

Once again, to grab the links and resources from today’s episode, just head over to youstaywealthy.com/184.

Thank you, as always, for listening and I’ll see you back here next week.

Disclaimer

This podcast is for informational and entertainment purposes only and should not be relied upon as a basis for investment decisions. This podcast is not engaged in rendering legal, financial, or other professional services.