Bonds are down 20%+ over the past three years.

Meanwhile, risky asset classes (like U.S. stocks) are UP ~30% during the same period.

- What the %@#! is happening to bonds right now?

- Why are safe asset classes down double digits while risky asset classes scream upward?

- Should retirement investors consider changes?

- Are money market funds and CDs a better solution than bond funds?

- And what might all of this mean for the future of bond investing?

I’m answering these questions (and more!) in this two-part series on bonds.

Need Tax + Retirement Planning Help?

We specialize in helping people aged 50+ lower taxes, invest smarter, and (safely) create a retirement paycheck.

Our Free Retirement Assessment™ will answer your BIG questions and help you properly evaluate our firm.

Click the banner below to learn more. 👇

Listen To This Episode On:

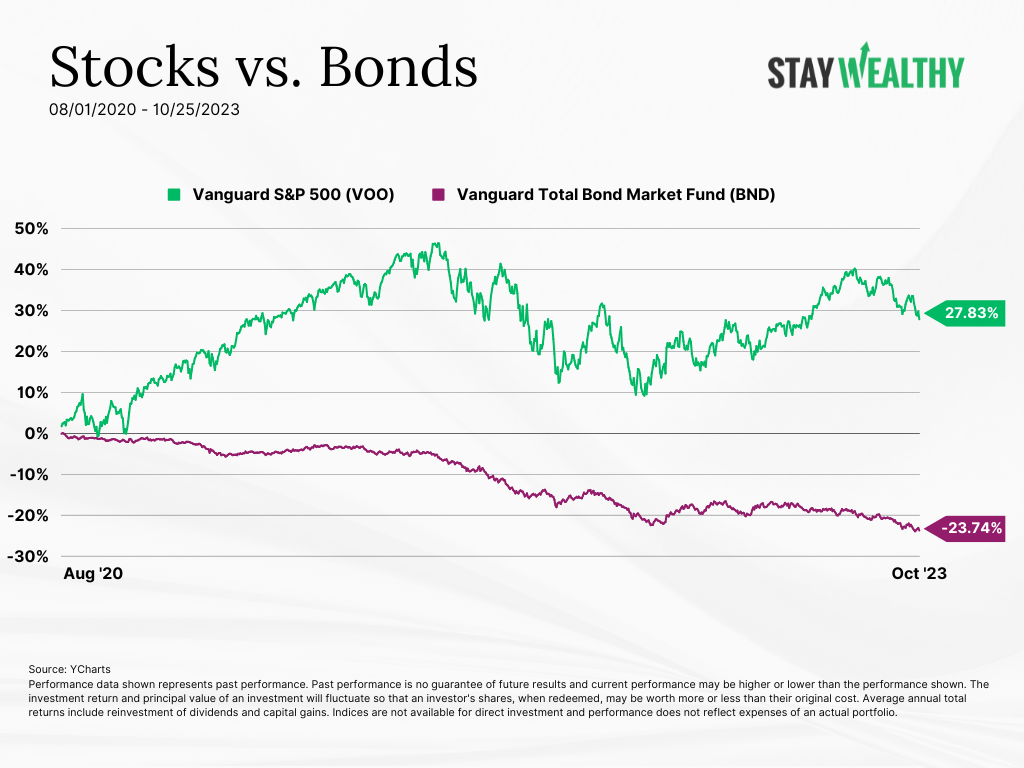

Stocks vs. Bonds (Aug 2020 – Oct 2023)

When You’re Ready, Here Are 3 Ways I Can Help You:

- Get Your FREE Retirement & Tax Analysis. Learn how to improve retirement success + lower taxes.

- Listen to the Stay Wealthy Retirement Show. An Apple Top 50 investing podcast.

- Check Out the Retirement Podcast Network. A safe place to get accurate information.

+ Episode Resources

📬 Want more retirement and investing content? Join thousands of listeners and subscribe to the Stay Wealthy Retirement Newsletter!

- Stay Wealthy 4-Part Bond Investing Series:

- Should Retirement Savers Own Bonds? [Stay Wealthy]

- Bond Duration Hypothetical Example [Dimensional]

- The Six Biggest Bond Risks [Investopedia]

- Vanguard Total Bond Market Index Fund [Vanguard]

- Vanguard Long-Term Treasury Fund [Vanguard]

- The Costs of Buying/Selling Individual Bonds [SSRN, Harris]

- Why Bond Funds Aren’t Necessarily a Losing Proposition in Rising Rate Environments [Kitces]

+ Episode Transcript

Taylor Schulte: Since August 1st of 2020, the Vanguard Total Bond Market Fund is down 24%. Even worse, the Vanguard Long Term Treasury Bond Fund is down 46%. And if those losses aren’t enough to cause frustration, the U.S. stock market is up 37% during this same three-year time period.

What the BLEEP is happening to bonds right now? Why are safe asset classes down double digits while risky asset classes scream upward? Should retirement investors make changes to their bond portfolio? Are money markets and CDs a better solution than bond funds? And what might all of this mean for the future of the bond market?

Welcome to the Stay Wealthy podcast! I’m your host Taylor Schulte and today I’m kicking off a two-part series to help answer these questions. I’m also sharing an actionable tip for improving your asset allocation if you’re struggling to determine what to do with your bonds in this current environment. For all the links and resources mentioned today, head over to youstaywealthy.com/203.

Part 1: What the %@#! Is Happening to Bonds

Shortly after the bond market peaked in August of 2020, I published a 4-part podcast series breaking down this asset class. I covered the pros and cons of individual bonds vs bond funds, the primary drivers of bond returns, why holding bonds to maturity isn’t always prudent, and how to invest in bonds.

If you want to revisit that series, I’ll link to it in today’s show notes. But I’m also going to share some of the research from that series here today to help support some of the big questions retirement investors are asking about bonds. So, if you don’t feel like going back into the archives, this short two-part series will provide you with the cliff notes.

Ok, to kick off part one today, let’s first quickly revisit what bonds are and why someone would want to include them in their portfolio.

So, when you buy a stock, you’re taking an ownership stake in the company you’re investing in. A very, very, very small ownership, but an ownership nonetheless.

Bonds, on the other hand, are loans. It’s kind of confusing, but when you BUY a bond, you’re actually loaning your money to someone – a corporation, municipality, or the government. In return, they’re paying you an interest rate during the term of your loan and, if all goes as planned, they will return your original loan back to you at the end of the term or maturity.

For example, you buy a 5-year $100,000 bond issued by ABC corporation that’s paying 5%. In this oversimplified example, ABC corporation will pay you 5% every year for 5 years (so a total of $25,000) and then return your original $100,000 back at the end of year 5.

Now, the interest rate you receive on the bond you purchase will depend on the risk profile of the company or institution you’re loaning your money to. Smaller, unknown corporation needs to borrow your money to fund their operations? They’ll pay you a higher interest rate to compensate you for that risk. That risk, of course, is that they don’t make it and you don’t see your original loan ever again.

With a basic understanding of what bonds are, let’s move into why someone might buy and own bonds as part of their investment strategy. In short, there are three reasons:

Number 1, attempt to outsmart the markets and earn a quick buck. Not all that different than a stock trader.

Number 2, for others, bonds are used to improve risk-adjusted returns during the accumulation phase of life. In other words, sprinkling in some bonds to a diversified portfolio can actually reduce risk while improving long-term returns over long periods of time.

Number 3, for my clients like mine who are in retirement or close to it, high-quality bonds are used primarily as a diversifier or stabilizer in the portfolio, not necessarily to boost returns. If a client needs or wants higher long-term returns, we would allocate more to stocks than bonds. As always, the more risk you take, the higher of a return you can expect.

Speaking of risk, just like stocks, bonds (and bond funds) contain different risk profiles that investors need to be aware of. There are risky bonds, safe bonds, and everything in between.

For example, corporate and municipal bonds typically pay higher interest rates (aka yields) and have higher expected returns than US treasury bonds. And that’s because, well, they’re riskier.

Unlike treasury bonds, corporate and muni bonds contain additional risks such as credit and liquidity risk.

In other words, there is a risk that the corporation you loaned money to can’t pay it back or they’re going through a tough time when you need or want to sell your bond and can’t get the price you were hoping for.

Once again, to compensate you for these risks, the issuers will typically pay you a higher interest rate. Not all that different than you commanding a higher interest rate when loaning money to a friend who can’t keep a job or has a bad track record of paying loans back. You would want to be compensated fairly for taking that extra risk.

In addition, the more risk you take with bonds, the more they begin to behave like stocks during catastrophic events. And during catastrophic events – especially when taking withdrawals from your portfolio to fund retirement expenses – it’s critical to have proper diversification.

It’s critical to own an asset class (or asset classes) that have low correlation to broad-based stocks. In other words, you want something in your portfolio to help stabilize things and maybe even earn a positive rate of return when traditional stocks collapse.

In the academic world, the technical term for this is Crisis Alpha. And, historically, during catastrophic events, AAA-rated US treasury bonds have produced significantly higher Crisis Alpha than their riskier counterparts.

Like any investment…stocks, real estate, or even cash…the reason for owning bonds, and the types of bonds an investor chooses to own, depends on the investors risk profile and, more importantly, their long-term goals. Because, as previously mentioned, bonds are not riskless.

Even safe, US Treasury bonds, bought and held to maturity contain risks. They don’t necessarily contain credit and liquidity risk like corporate or junk bonds, but they contain interest rate (or duration) risk, inflation risk, and reinvestment risk. And we’re seeing some those risks appear in real-time right now, even with the highest rated bonds in the world.

Since August of 2020, intermediate term treasury bond funds are down between 15% and 20%. Why are safe US treasury bonds down 15-20% in the last three years? Interest rate risk (aka duration risk). Let’s explore what this means.

So, while the Fed doesn’t control bond yields, it does influence them. And in response to the Fed rapidly raising the fed funds rate in recent years, bond yields, have followed suit. And when bond yields rise, their prices fall – there’s an inverse relationship that most investors are aware of. That is interest rate risk.

This inverse relationship is talked about a lot but it’s not typically explained very well. Why exactly would bond prices fall when interest rates (or yields) rise?

Well, let’s say, last year, I bought a 5-year $100,000 treasury bond that pays me 2%. And then, unfortunately for me, interest rates jumped shortly after buying my bond, and here in 2023, one year later, all new 5-year treasury bonds issued in the market are now paying 4%.

I’m stuck with my 5-year bond paying 2% while everyone else gets to buy 5-year bonds at 4%. All of sudden, my bond doesn’t look too attractive. If I try to sell you my bond for the $100,000 I paid for it, you wouldn’t do it, knowing that you can just go buy a newly issued 5-year bond that pays double what mine is paying.

The only way you might consider buying my bond is if I sell it to you at a discount and realize a loss on my investment. For example, instead of selling it to you for the $100,000 I paid for it, I might have to sell it to you for $85,000.

You buying it for $85,000 would be a good deal, because if you hold it until maturity, you’ll get paid back the original $100,000 on top of the 2% interest you collected along the way. The same logic and math applies to bond funds, it’s just occurring across thousands of bonds instead of one bond.

So, if you bought your bond fund in 2020, and tried to sell it today, you would have to sell it at a discount and realize a loss, just like I did in my example. The difference with the bond fund, which we will dig into more here in a minute, is that your bond fund yield is higher, because bonds are regularly maturing inside the fund and being reinvested at today’s current rates.

So if you don’t panic and sell it and take a loss, you will receive today’s higher yield and begin to recoup those paper losses.

Quick side note…some people have questioned why anyone would have owned bonds in their portfolio 3+ years ago when interest rates were so low. With their 20/20 hindsight glasses on, they said it was obvious that interest rates, and in turn bond yields would go up, and therefore bonds were guaranteed to fall in price.

However, as I shared in my episode on bonds titled “Should Retirement Savers Own Bonds”, not even the Fed knew that the Fed was going to raise rates to this degree. I know this because the Fed publicly shares their targets for not just GDP and inflation but also interest rates.

And in June of 2021, the Fed projected that the fed funds rate would be between 0.1 and 0.6 in 2022 and 0.1 – 1.6 in 2023. For context, today, the fund funds rate sits at 5.33% – more than twice as high as their expectations.

While some market timers might have had their crystal ball working perfectly, and successfully predicted all of the events that would follow a global pandemic that caught everyone off guard, most people, including the Fed themselves, did not see this rapid spike in interest rates coming. And this quick, unpredictable pivot in interest rate policy really shocked the markets, sending bond yields higher and bond prices lower.

So, yes, in hindsight, it’s easy to kick ourselves for owning bonds and it’s easy to say that we should have seen this coming, sold our bonds, and stuffed everything under the mattress. But that would require a crystal ball, a crystal ball that not even the Fed had access to.

And then, of course, we have to make sure that our crystal ball is right twice. We not only need to have sold our bonds at the perfect time, but we then need to know when to buy back in.

For some reason, it’s easy for many investors to acknowledge that timing the stock market is impossible, and therefore agree that it’s best to buy and hold low-cost index funds versus actively trading stocks. But when it comes to bonds, cash, and CDs, investors seem more confident about when to shift in and out of these “safe” asset classes.

And while they are, typically, safe asset classes – or at least safer and less volatile than stocks – they are far from simple, and an investor can get themselves into just as much trouble trying to time bonds as they can with stocks.

Ok, quick recap before we go any further:

Not all bonds are equal. There are risky bonds, safe bonds, and everything in between.

The reason for owning bonds depends on the investor and their unique goals.

Bond yields have spiked rapidly, sending bond prices down.

Trying to time the bond market is just as dangerous as trying to time the stock market.

As always, while not everyone shares my philosophy, I personally do not believe anyone has a crystal ball that consistently predicts the future. And I especially do not believe anyone has a crystal ball that predicts it twice.

So, I’ve mentioned a couple of times now that bonds are down double digits in the last three years because interest rates (or yields) have spiked. In my experience, most investors get stuck on the former (bonds down) and don’t consider the latter (yields are up).

Yes, your safe intermediate treasury bond fund has dropped in price over the last three years, but it also now has a higher yield. Higher yield means higher future returns. And the great thing about investing in US treasuries versus other riskier bonds is that their risk/return profile is fairly predictable.

More specifically, the duration of the treasury bond – or treasury bond fund you invest in – tells you everything you need to know about how it will respond to rising yields and it’s future expected returns. While the same math applies to other bonds, there are other unpredictable risks we touched on earlier that can disrupt that math, so it’s not as reliable.

So again, the duration of treasury bonds or a treasury bond fund tells us everything we need to know about how it will respond to changes in bond yields. Put simply, bond duration is a way of measuring how much bond prices are likely to change if and when yields move.

For example, if yields were to rise 1%, a bond fund with a 5-year average duration would likely lose approximately 5% of its value. If the duration was longer, the loss would be greater. If duration was shorter, the value lost would be lower.

Of course, just like stocks, you can’t have your cake and eat it too. If you want less interest rate risk, you have to accept lower yields and returns. Once again, how a bond portfolio is constructed depends on the risk/return profile and goals of an investor. There’s no free lunch here.

By the way, to find the duration of your bond fund, just head to the fact page for the fund you own or punch the ticker symbol into Morningstar.com. It’s a transparent number that’s very easy to locate and is something every investor who owns bonds or bond funds should take note of.

Ok, with that basic explanation of the relationship between bonds and changes in interest rates, let me share a quick example that isn’t too far from the current situation we’re experiencing right now to help illustrate how bonds work and how we can set proper expectations with our bond investments.

Let’s say I put $100,000 into a bond fund that is yielding 1% and has a duration of 5 years. And let’s say there are two potential scenarios that could occur after I make this investment.

In scenario 1, interest rates stay low forever. Covid never happens, we remain in this low-interest rate environment, and I just continue to clip my 1% yield. In this scenario, by the end of year 5, my bond fund investment slowly grows from $100,000 to $105,000 (and change). I didn’t make much money but also didn’t suffer through any volatility or experience any losses.

In scenario 2, the economic environment changes rapidly on me. The Fed changes their low interest rate policy overnight, the yield on my bond fund immediately jumps to 4%, and then remains at 4% for the next 20 years. Because my bond fund has a duration of 5, the immediate spike in yields, causes my $100,000 investment to drop to $86,385 on the first day of trading.

In one day, I lose almost $14,000 in my safe US treasury bond fund. But I don’t need to access the money. I bought this fund because my time horizon is greater than 5 years for this investment bucket. So, while losing $14,000 in one day isn’t fun, I’m aware that my bond fund is now paying 4%.

Now that I’m earning a higher interest rate, my investment begins to claw back and ends year 1 at close to $90,000. By the end of year 2 it ends the year just over $93,000, year 3 at $97,000, year 4 at $101,000, and finally at the end of year 5, my original investment that lost $14,000 on day one is worth $105,000 and change.

If you’re following, that’s the exact amount that I had at the end of 5 years in scenario 1 where interest rates remained at 1% and never moved. In other words, my breakeven point was at the 5 year mark, the duration of my bond fund. It was a bumpy ride to get there, but that was a transparent risk I knew I was taking when I purchased a bond fund with a 5 year duration.

So why would I opt for Scenario 2? Why would I willingly buy a bond fund with a 5 year duration that would take me on a wild ride only to break even with Scenario 1 in 5 years? Because I’m a long-term investor and, in Scenario 2, I have a bond fund paying 4% that crossed the breakeven point and is now compounding at that rate every year.

By the end of year 10, my bond fund in Scenario 2 is worth almost $128,000. The same fund in Scenario 1 that’s still slowly slipping 1% is only worth $110,000. And by the end of year 20, Scenario 2 is worth roughly $190,000, while Scenario 1 just barely crossed $120,000.

Not only did I end up with a healthy rate of return during that time period, but I didn’t have to spend my valuable time jumping in and out of individual bonds, praying that reinvestment risk didn’t disrupt my target return. We haven’t talked about reinvestment risk yet, but this is another danger that individual bond (and CD) investors face.

Reinvestment risk is the risk of having to reinvest proceeds of a bond or CD that’s maturing at a lower rate than what the funds were previously earning. With a low-cost, high-quality bond fund, I own thousands of bonds at basically no cost that are all constantly maturing and being reinvested at new, current rates.

If I own a handful of individual bonds, I have to wait for my next bond to mature before I can reinvest – and who knows what rates will be doing while I wait for that next maturity date. Even worse, my bonds could be “callable” and the issuer could give me my original loan back early because rates dropped and they’re no longer interested in paying me the original interest rate.

So, I ended up with a much healthier return in scenario 2 over the long-term without doing much other than staying the course after starting in a $14,000 hole. But the point here is not to make an argument for taking risks with your bonds, and suggest that it doesn’t matter if you experience double-digit losses in the near-term (like many bond investors are experiencing now).

The point is that investors need to match their risk and bond duration with their investment time horizon. In other words, if an investor has a 3-year time horizon for a particular bucket of money, then they shouldn’t allocate that bucket of money to a bond fund with a duration of 5. An investor’s time horizon should match up with (or be greater than) the duration of your bond investment.

Going back to where we started this episode, the Vanguard Total Bond Market Fund, one of the largest bond index funds at close to $300 billion in assets, has an average duration of about 6 years.

So, if an investor bought this fund in August of 2020, and currently finds themselves down 24%, it’s worth highlighting that this was a transparent risk they knew (or should have known) existed. And, hopefully, their time horizon for the money invested in this fund is greater than 6 years.

Because if it is, then they should be excited about the current 5% yield and higher future expected returns and they should do their very best to ignore the performance here in the short run. Not all that different than investing in the stock market.

Most investors know that anything can happen to stocks within a 10-15 year time period, and wouldn’t (or shouldn’t) take risk in the stock market with money they need access to in the short term. And this is precisely why diversification is so important. In addition to ensuring that everything we own isn’t highly correlated, we want to ensure that we have investments earmarked for short, intermediate, and long-term needs.

Now, just because we have these proper investment buckets established, doesn’t mean they always perform how we would expect them to in the short term. Sometimes those long-term risky investments do well in the near-term and we can rebalance out of them to fund living expenses.

Other times, they might go on a wild ride, forcing us to stick to our plan and lean on our war chest of cash and bonds to fund near-term living expense needs. It’s anyone’s guess how each asset class will perform month by month year by year, which is why diversification and matching our time horizon with our different investment buckets is so important.

It’s also why I’m an advocate for Total Return Investing. Instead of solely relying on yield, a total-return investing strategy allows investors to spend from appreciation in the portfolio, rebalancing the different holdings based on current-year performance.

In summary, if your investment grade bond fund has lost money in recent months or years, it’s not because you made a bad investment or that bonds are bad or that you should sell it all and buy bank CDs instead – it’s just that the risks contained in the bond fund you own – risks that should have been taken into consideration – showed up, and they showed up rather quickly, catching many investors off guard.

We’ve experienced rising rate environments before, but they haven’t always been this quick and extreme. For example, in 1950, long-term US government bonds yielded just over 2%. By 1960, yields jumped to 4.5%, by 1970 they jumped to 10%, and by 1981, they reached 15%.

So, yields jumped from 2% to 15% in roughly 30 years. Even knowing what you know now, you’d likely guess that bonds lost a lot of value during this time period of rising rates. But that’s not the case. Long-term government bonds had an average annual return just over 2%, and had a cumulative return just over 90% during that time period.

As Ben Carlson put it, this period of time was more of a death-by-a-thousand-cuts. The change in rates was gradual, which is not what we’ve experienced in the last three years.

And personally, I’m not sure what’s worse or what would be easier for an investor to manage from a behavioral perspective. Investing is hard, no matter what way you spin it. Long-term investors are regularly hit with new and different challenges that cause them to second guess their approach, try something new, and make, potentially, irrational changes to their portfolios.

But, unlike most areas of our life, when it comes to investing, taking action and making dramatic changes to our portfolios typically hinders our long-term goals. As John Bogle once said,

“Don’t do something, just stand there.”

But let’s say an investor feels inclined to do something. Let’s say they don’t have the proper portfolio and the bonds they own don’t match up with their risk, time horizon, and retirement goals. What should those investors do to get their investments back in line? And what about money markets yielding 5%?

Is that a good bond alternative for those that don’t want to take duration risk? Finally, what does the future of bond investing look like? Does the current interest rate environment shift how retirement investors should approach this asset class going forward?

I’ll be tackling those questions and more next week in part two of this two-part series on bonds.

To grab the links and resources supporting today’s episode, just head over to youstaywealthy.com/203. Thank you, as always, for listening and I will see you back here next week.

Disclaimer

This podcast is for informational and entertainment purposes only and should not be relied upon as a basis for investment decisions. This podcast is not engaged in rendering legal, financial, or other professional services.