“Just buy the index.”

It’s the simple advice that built your wealth and got you to the finish line.

But here’s what often gets overlooked by investors:

The strategy that got you to retirement won’t necessarily keep you there.

When you switch from saving to spending, the math changes.

Suddenly, relying on a “simple” S&P 500 strategy exposes you to risks that didn’t matter when you had a paycheck.

In this episode, we cover:

- The Simplicity Trap: Why “decision fatigue” lures smart retirees into risky, overly concentrated portfolios.

- S&P 500 Reality Check: Why the “safe” default option is actually dangerous for your retirement income.

- The “Flatline” Defense: How to build a retirement portfolio that protects your purchasing power during downturns.

- Beyond Investing: How to align your investments, taxes, and legacy for true peace of mind.

If you are approaching retirement and wondering if your “set it and forget it” strategy is enough to last a lifetime this episode is for you.

Listen To This Episode On:

When You’re Ready, Here Are 3 Ways I Can Help You:

- Schedule a Free Retirement Strategy Session. Get your questions answered + learn how we can help you improve retirement success and lower taxes.

- Listen to the Stay Wealthy Retirement Show. An Apple Top 50 investing podcast.

- Join My Retirement Newsletter. Weekly retirement and investing tips (delivered to our inbox!)

+ Episode Resources

- International Stock Outperformance When U.S. Stock Returns Are Low

- The 1970’s Hypothetical Example

- The Lost Decade Hypothetical Example

- The Lost Decade 5% Withdraw Hypothetical Scenario

- Guyton Guardrails – FPA Academic Paper

- How to Invest During a Lost Decade

- 10% Average Stock Market Returns

- Additional Disclosures

+ Episode Transcript

Here’s something I’m experiencing more and more often. A friend, family member, or even a potential new client shares with me that most of their nest egg is sitting in the S&P 500. When I ask why, the answer is almost always the same. It’s simple, low cost, and it’s outperformed just about everything else for decades. Some even quote Warren Buffett, who’s famous for saying that a low-cost S&P 500 index fund is quote, the best investment most people can make.

And honestly, I get it, I really do. The S&P 500 has been a great investment. It’s easy to access and it’s practically free to own.

And after decades of saving and investing, the last thing most people want right as they approach retirement is to make a mistake, a mistake that can put their plan in jeopardy. So naturally, they cling to what feels familiar and proven. They stick with the solution that worked so well for them during their working years, the solution that successfully got them to the finish line, because why fix something that doesn’t seem broken?

But here’s the thing, that seemingly smart choice is often driven by misinformation and or overwhelm, not logic and evidence, and it’s exposing retirees to the very risks they’re trying to avoid.

So in today’s episode, I’m challenging Warren Buffett’s advice and sharing real-life data to prove why a properly built portfolio is not just a good idea, it’s essential for retirement success.

Welcome to another episode of the Stay Wealthy Retirement Show. I’m your host, Taylor Schulte, and every week, I tackle the most important financial topics to help you stay wealthy in retirement. And now on to the episode.

The S&P 500 Trap: Why the “Safe” Choice Is Actually Risky for Retirees

I’ll let you guys in on a little secret today. One of my guilty pleasures is watching TV in bed to fall asleep. My wife especially loves it when I spend 15 minutes clicking through every app, checking out all of my options, looking for something new to watch, only to end up rewatching yet another episode of Seinfeld for the hundredth time.

Behavioral experts call this the paradox of choice. You see, when we’re faced with too many options, we actually don’t feel empowered. We feel overwhelmed, and we end up reverting back to something familiar. And that’s exactly what’s happening with retirement investing today. You log in to your account and you’re hit with 50, 100, sometimes thousands of investment options.

Growth, value, small cap, large cap, international, bonds, mutual funds, exchange traded funds, closed end funds. It’s understandably exhausting. So, as a result, most people freeze and default to the thing that they recognize, or the thing that’s been performing best recently, or the thing they heard the greatest investor of all time recommend.

And for most of this century, that’s been the S&P 500. Compared to the thousands of other confusing options, it feels simple and smart and safe, but in reality, it’s actually exposing you to the very risks you’re trying to avoid, especially in retirement when your portfolio has to consistently provide a paycheck. What many people don’t realize is that proper diversification, and proper is the key word here, proper diversification can actually reduce risk and improve long-term returns while also being simple and low cost.

You don’t have to choose between simple and smart. You can have both. And in a moment, I’ll walk you through the data that proves it. But first, let’s quickly discuss why investing most of your savings in the S&P 500 may be far riskier than most retirees realize.

To start, an S&P 500 index fund owns 500 of the largest companies in the United States. Now, on the surface, that sounds quite diversified, especially compared to your stock-picking neighbor. But here is the primary problem. The S&P 500 is made up of only US stocks.

Meanwhile, there are over 18,000, yes, 18,000 other publicly traded companies outside of America, representing 35% of the global equity market. By concentrating everything in a single country, you are introducing a very real form of geographic risk.

Now, I know what you might be thinking, but Taylor, the US stock market has been the world’s top performer for decades. Why would I bet against this country? And technically, yes, you are right.

US large-cap stocks have delivered higher returns with less volatility than international markets over the last 50-plus years. But here’s where that logic breaks down, especially for retirees. Investment returns are lumpy. Those attractive long-term averages that you see in the headlines, they don’t show up neatly every single year. In fact, since 1926, the S&P 500’s long-term average annual return, which most are familiar with, has been about 10%.

However, across all 10-year rolling periods over the past 100 years, it only delivered 10% or more per year, 50% of the time. In other words, investors should expect real-world 10-year results to swing above and below that 10% average far more often than they match it exactly. Once again, investment returns are lumpy.

Sometimes US stocks skyrocket, sometimes they collapse, and sometimes they go nowhere. And that inconsistency creates two big problems. First, investing is highly emotional. As Charlie Ellis once said,

“the average long-term experience in investing is never surprising, but the short-term experience is always surprising.”

And when your portfolio constantly surprises you, it becomes much easier to panic and make costly decisions. For retirees, those surprises aren’t just stressful, they’re incredibly dangerous. Panic selling and stuffing everything under the mattress or ditching a strategy to chase the next popular investment trend can quickly derail your entire plan. Smart global diversification helps smooth out that ride and in turn dramatically improves your odds of staying invested for the long run.

And staying invested for the long run is critical in retirement for those who are relying on their portfolio for predictable, sustainable income.

Second, when you’re retired and taking regular withdrawals, your S&P 500 only portfolio lacks assets that zig when US stocks zag. And that matters a lot because once you’re drawing income from your portfolio, the order of your returns becomes just as important as the returns themselves. If your US stocks drop sharply while you’re in retirement and you’re forced to sell shares at a loss to fund your expenses, you could permanently reduce your future spending power. That’s what’s known as sequence of returns risk.

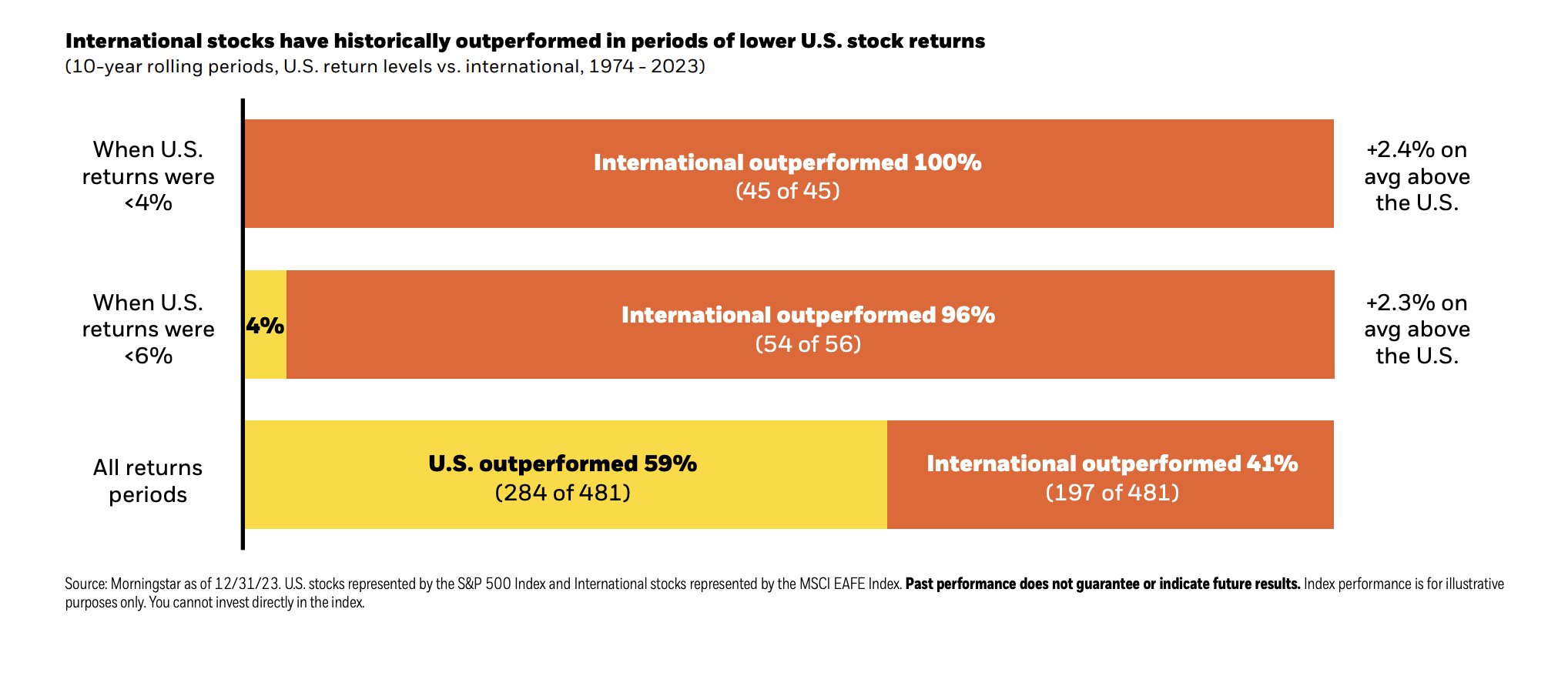

Global diversification helps buffer against that. In fact, let’s revisit one of my favorite statistics I’ve shared on the show before that highlights the benefit of global diversification for retirees. Since 1974, as far back as the data goes, in every single year when US stock returns were below 4%, international stocks outperformed by an average of 2.4%. I’ll say that again so it sticks. In every single year when US returns were less than 4%, international markets outperformed, not just by a little, but by an average of 2.4% per year. That kind of diversification is not theoretical. It’s practical.

It gives you something or some things in your portfolio to sell when US stocks go down, allowing you to fund your retirement income without locking in losses and without stress or worry.

And I’m about to show you how it’s helped retirement investors through two major storms by showing you the exact returns of the S&P 500 versus a properly diversified global portfolio.

Diversification Benefits

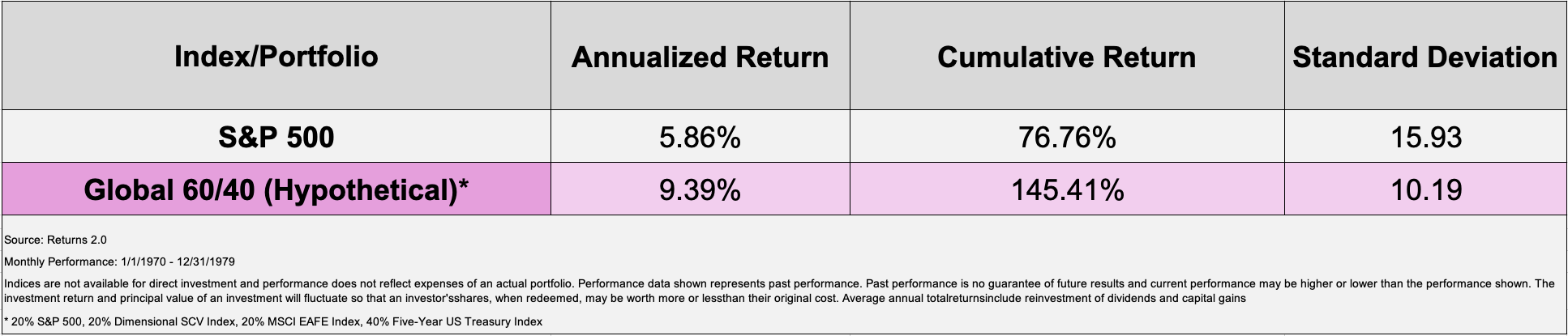

The first major storm to review took place in the 1970s. Now, since data and investment options were more limited back then, for this comparison our hypothetical diversified portfolio looked like this. 20% in the S&P 500, 20% in small-cap value stocks, 20% in international developed stocks, and 40% in plain vanilla 5-year treasury bonds.

So from 1970 through the end of 1979, the S&P 500 delivered a total return of about 76%, roughly 6% per year on average. Not terrible, right? On paper, maybe, because here is the problem. Inflation averaged nearly 7% per year during that same decade. So after inflation, S&P 500-only investors actually lost purchasing power even though they generated 6% average returns.

Their so-called growth portfolio didn’t grow at all in real terms after inflation was factored in. On the other hand, our hypothetical globally diversified portfolio averaged about 9.5% per year during this same time period. After inflation, that means globally diversified investors not only preserved their purchasing power, they grew it. Even through one of the most difficult decades for retirees in history, diversification turned a challenging 10-year period into a survivable one. A few decades later, the world changed significantly, but the lessons did not.

Diversification was still the retirees’ best shock absorber, and it was about to be tested again. It was the early 2000s when another storm hit, one that everyone listening probably remembers all too well. And this time, investors had a few more tools at their disposal. So instead of the simple 1970s mix, our updated diversified portfolio builds on the same foundation but adds real estate, emerging markets, and international value stocks to the portfolio.

So from 2000 to 2009, the S&P 500 lost about 9% in total, a negative 9% total return with dividends reinvested over 10 full years, commonly referred to as the lost decade. And it was not just a slow erosion. The S&P 500 actually dropped more than 50% twice in those 10 years. Two devastating crashes in a single decade. That’s the kind of volatility that can cause serious stress and anxiety, and even worse, derail a retirement plan overnight.

Now if you had mixed in some bonds, say a basic 60% S&P 500, 40% bond portfolio, you would have absolutely weathered this storm better. That negative 9% loss would have turned into roughly a 33% total gain with a simple 60-40 allocation. An improvement for sure, but a roughly 3% average return in the face of inflation that averaged around 2.5% was likely not enough to give you the ability and confidence to maintain your desired lifestyle in retirement.

Now here’s where things get interesting. Our hypothetical global portfolio, the one with exposure to multiple evidence-based asset classes and geographic regions, returned well over 100% during that same time period. That’s not a rounding error. That’s the difference between barely keeping your head above water and doubling your money, i.e. your purchasing power, through one of the worst decades in market history. And this hopefully helps to highlight the danger of single-country concentration. Because when, not if, but when, the US hits a rough patch, your entire portfolio suffers.

But with a properly built, globally diversified portfolio, you’ve got multiple engines driving your returns. For retirees, that means a smoother ride and consistent income even when one part of the market is struggling. And perhaps most importantly, it means dramatically lowering the risk of running out of money in retirement. Let me explain what I mean by sharing one of my favorite hypothetical, yet very relatable scenarios with you.

Retirement Game Changes

Imagine you retired in the year 2000 with a $1 million portfolio. You start withdrawing $50,000 per year from your investments, simply adjusting your annual withdrawals for inflation. A pretty typical scenario for a retiree who wants to enjoy retirement and doesn’t want to die with a pile of money. So if you followed this spending plan and invested your $1 million nest egg in a low-cost S&P 500 index fund, the simple proven choice, your portfolio would have been completely drained all the way down to $0 in just 16 years.

If instead you built a properly diversified global portfolio, one that included small-cap and value stocks, international exposure and real estate, you would have ended that exact same period with more money than what you started with. That’s the power of smart diversification in retirement. When you’re still in your working years and accumulating money, you can more easily ride out volatility and challenging times.

You can take a simpler, possibly more concentrated investment approach, and you can ignore headlines, stay the course, and since time is on your side, you can patiently wait to recover from these storms. But once you start taking withdrawals from your portfolio, the game changes. Every dollar you pull from a falling asset class is a dollar that cannot recover later, which is why proper diversification becomes absolutely critical in retirement.

So, to be extra clear, what I’m sharing with you today is not about trying to outsmart the market or boost returns. It’s about protecting your paycheck, preserving your peace of mind, and giving you confidence to enjoy the retirement that you work so hard for. When I share this data with retirees or soon-to-be retirees, it helps them see how true diversification has performed through catastrophic events, and their perspective completely shifts.

They realize that safe is not necessarily about owning what’s familiar or sticking with the investment plan that got them to the finish line. It’s about building an academically sound portfolio that stays strong when the world doesn’t.

Holistic Financial Plan

Still, even the strongest portfolio is not the full story, because once you retire, new variables start to appear. Taxes, income timing, health care costs, legacy goals. Each one has the power to undo the progress your portfolio makes if it’s not coordinated. True confidence does not come from investments alone. It comes from connecting every piece of your financial life so it all works together. But even after learning and understanding this, many retirees still treat their investment strategy like it’s their entire plan. They invest in a diversified portfolio, they hit set it and forget it, and they assume they’re done.

Then reality sets in. Taxes start eating away at their returns, RMDs push up Medicare premiums, and that perfect portfolio doesn’t feel so perfect anymore. True retirement success, in my experience, does not come from a single chart or even a perfectly designed, perfectly diversified portfolio. It comes from connecting all the pieces of your financial life, so they work together instead of against each other.

At my firm, we use a proven four-step framework to connect the four big levers in retirement, taxes, income, legacy and investments, into one single coordinated plan. The goal and intention behind building this framework is to avoid solving problems in isolation, because in retirement, every tax decision affects your income, which affects what you can safely spend, and ultimately what you can leave behind.

And many people, including financial professionals, want to start the discussion or planning process by addressing investments. I get it, talking about investments is way more fun and interesting than talking about Medicare IRMAA or RMD planning. But in our framework, investment strategy is intentionally the last step. This way, by the time we get to investments, the portfolio is backed by a tax-smart, income-aligned, legacy-aware plan.

In my experience, this process and framework not only improves the odds of long-term retirement success, it also removes a lot of the emotion and guesswork, and it turns investing from something stressful into something strategic and repeatable.

Portfolio Construction

Now, while every allocation is unique to a client’s needs and goals, at a high level, our globally diversified portfolios contain the exact asset classes that I referenced in the hypothetical scenarios today. REITs, emerging markets, large and small international stocks, large and small US stocks, all with a little extra weighting on companies with profitability, quality and value characteristics.

We don’t include these asset classes because they sound important, but because academic research has proven that they complement each other in a diversified retirement portfolio.

When it comes to bonds, our goal is not growth, it’s protection and income. So we use a mix of high-quality US Treasuries and inflation-protected securities, and we ditch the riskier solutions like lower-grade corporate bonds. The right mix between these major asset classes helps to stabilize your income, dampen volatility, and keep your long-term plan intact when markets get noisy. It also supports the research that drives the retirement guardrail strategy.

For example, if you’re following the guardrails-based withdrawal strategy, have a $1 million portfolio, and need about $55,000 per year, the research points to an allocation of 65% global stocks, 25% bonds, and 10% cash. If you need more or less income from your portfolio, you would simply adjust your stock-bond mix up or down. You would allocate more to stocks for growth and higher withdrawals, and more to bonds for stability and lower withdrawals.

Again, to be extra clear, a portfolio like this that we’ve discussed is not about chasing or boosting returns. It’s about coordination and alignment with retirement goals. It balances healthy growth with downside protection, inflation defense, and tax efficiency all within a system that works together.

Plan for Confidence

When you properly connect all the pieces of your financial life, you stop managing your money in isolation and start managing it like a complete evidence-based retirement plan, one that gives you peace of mind and confidence.

As always, if you have any questions that you think I can answer, please send me an email at podcast@youstaywealthy.com. That’s podcast@youstaywealthy.com. I read and respond to every message, no strings attached. And if you’ve determined that you want professional help, or you’re looking for a second opinion, my team and I would be honored to have a conversation. You can learn more about scheduling a free retirement strategy session by visiting the link in the episode description right there in your podcast app.

Thank you for listening. And once again, to view the research and resources referenced in today’s episode, just head over to youstaywealthy.com/260.

Disclaimer

This podcast is for informational and entertainment purposes only, and should not be relied upon as a basis for investment decisions. This podcast is not engaged in rendering legal, financial, or other professional services.

{kind=link}

{kind=link}