You’ve finally made it to retirement!

But what if some of the choices you’re making right now are quietly pulling you back to work?

Every year, countless retirees are forced back into the workplace.

Not because they were reckless, but because they followed advice that sounded smart and safe.

In this episode, I’m sharing 7 of the most common retirement pitfalls that can derail even the best-laid plans.

I’m also sharing our Total Retirement System™—a comprehensive framework to ensure you retire once and never look back.

If you’re approaching retirement (or already there) and want to avoid mistakes that force people back to work, this episode is for you.

Listen To This Episode On:

When You’re Ready, Here Are 3 Ways I Can Help You:

- Get Your FREE Retirement & Tax Analysis. Learn how to improve retirement success + lower taxes.

- Listen to the Stay Wealthy Retirement Show. An Apple Top 50 investing podcast.

- Join My Retirement Newsletter. Weekly retirement and investing tips (delivered to our inbox!)

+ Episode Charts

+ Episode Resources

- Get Your FREE Retirement Assessment

- Guardrails Flexible Withdrawal Strategy

- Tax Effect on Dividends Can Be Up to 1.5% Per Year

- 80% of S&P 500 Companies Pay a Dividend

- Why the 4% Rule is Problematic and Overly Conservative

- Backtest: Retiring Into the Lost Decade (Paid Account Required)

- Long-Term Care Statistics

+ Transcript: 7 Retirement Pitfalls to Avoid

You’ve finally made it. You are retired.

But what if some of the choices you’re making right now are quietly pulling you back to work? Every year, countless retirees are forced back into the workplace. In some cases, it’s due to bad financial habits or economic events outside of their control. But for many, going back to work is a result of following bad advice—advice that sounded smart and safe on paper.

Welcome to the Stay Wealthy podcast. I’m your host, Taylor Schulte, and today I’m talking about retirement pitfalls. Specifically, I’m sharing 7 of the most common retirement pitfalls that can derail even the best-laid plans. I’m also sharing how to avoid them, so you can retire once and never look back.

To view the articles and research supporting today’s episode, just head over to youstaywealthy.com/242.

The Retirement Sustainability Trap

Most retirees focus on having ENOUGH to retire, but too many overlook what it takes to STAY retired.

And that’s a big problem.

Because retirement success is not just about hitting a savings number—it’s about managing dozens of small decisions that add up—decisions that either preserve your freedom or slowly chip away at it.

This is what I often refer to as the Retirement Sustainability Trap.

You make a few reasonable choices—a little extra withdrawal here, ignoring taxes there—and suddenly your carefully built plan starts to crack.

It doesn’t happen all at once. But over time, the cracks compound.

Eventually, you’re left with this painful question: “Do I need to go back to work?”

That’s why retirement planning isn’t just about reaching the finish line. It’s about knowing how to live on the other side of it.

And what I’ve found is that retirement sustainability isn’t about complex strategies.

It’s about avoiding pitfalls, and I’ve hand-picked 7 of the most common ones that increase the risk of forcing retirees back to work.

Let’s go through them now.

Pitfall #1: “Dividend Tunnel Vision”

Dividend investing sounds like the perfect retirement solution, especially when you see headlines that say things like:

“Buy income-producing stocks and make money while you sleep.”

But here’s the problem: That income isn’t free.

When a dividend is paid, a company’s stock price typically drops by the same amount.

And that’s because a dividend is simply a distribution of company profits.

A slice of the company’s value is being removed from its balance sheet and sent to shareholders like you.

You might feel richer because you saw a cash payment hit your account. But mathematically, when you receive a dividend, you’re in the same spot.

And it doesn’t stop there.

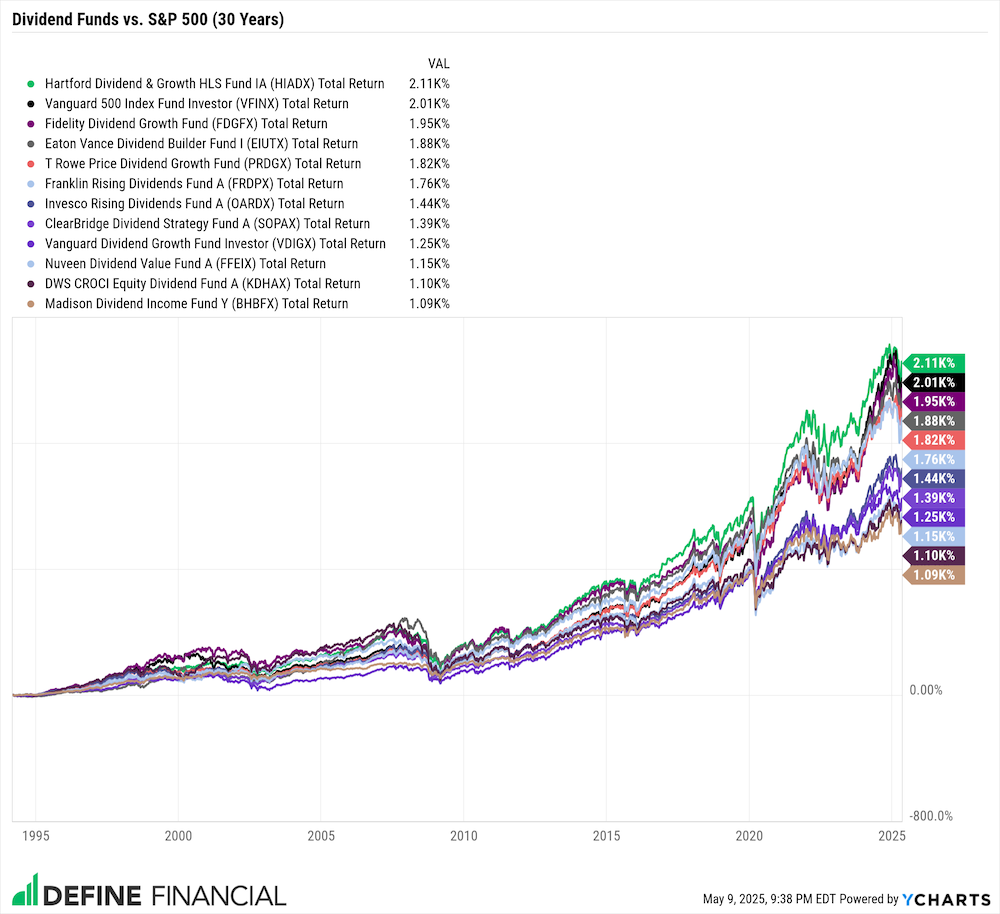

Many dividend-focused strategies charge significantly higher fees than broad-based index funds.

As a result, nearly 90% of the dividend-focused funds that survived the last 30 years have underperformed the basic, plain vanilla Vanguard S&P 500 fund.

Lastly, high dividend stocks can be a tax nightmare.

And that’s because you owe taxes on dividends earned in a taxable account every year—even if you don’t spend them.

Depending on your tax bracket, research has shown that dividend taxes can reduce your annual investment returns by up to 1.5% per year.

So, what should you do instead?

You should buy good companies at good prices and focus on total return, not yield.

Since 80% of S&P 500 companies pay a dividend, a properly diversified portfolio will naturally generate income.

But the current yield of a company or fund should NOT influence what you include in the portfolio.

If you want to dive deeper into dividend investing, check out the 4-part series I published last year on the podcast, which I’ll include in today’s show notes for quick access.

Pitfall #2: The Bond Risk Blind Spot

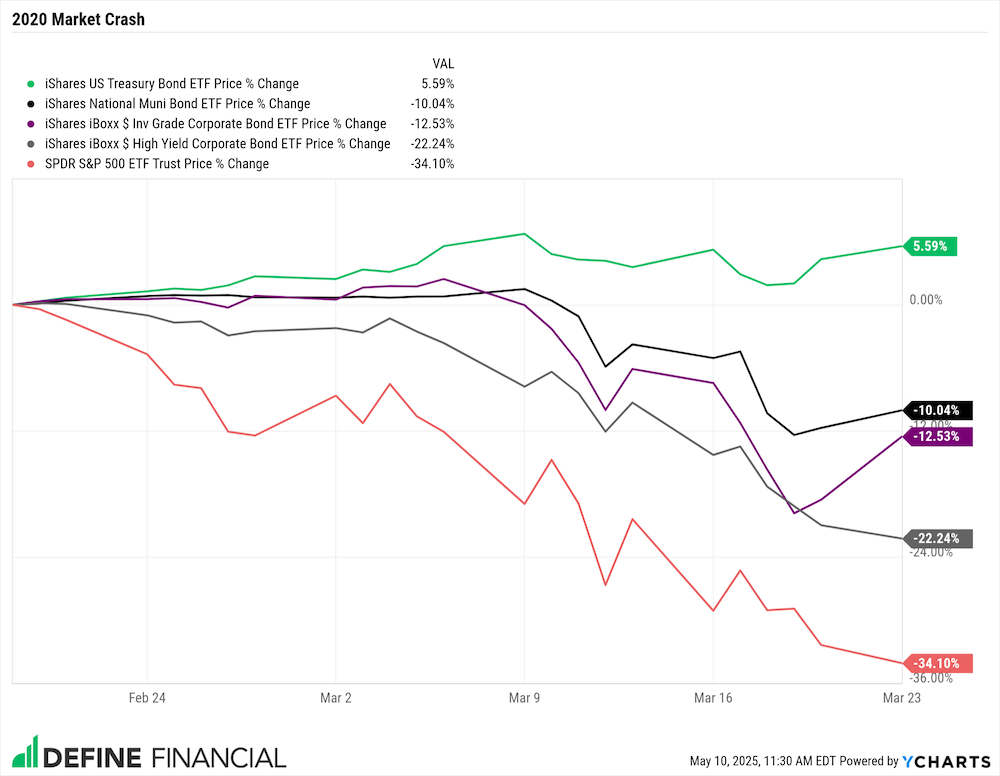

Contrary to popular belief, not all bonds protect you during market meltdowns.

For example, in 2020, the U.S. stock market dropped 34% in three short weeks.

During this same period, corporate and municipal bonds—two asset classes often thought of as safe—were also down between 10% – 20%.

Meanwhile, U.S. treasury bonds returned a positive 5.5% during this crash.

Retirees often chase higher-yielding bonds for the extra income, and that’s understandable.

However, those bonds are riskier and can fall in value right when you need them most.

We want our bonds to provide protection during catastrophic market events, especially in retirement when you are living off your nest egg.

And, historically, U.S. treasury bonds have done just that.

Sure, they might pay a little less interest, but they typically provide more stability, and that trade-off can be critical in retirement.

Pitfall #3: The Withdrawal Rate Gamble

You’ve likely heard of the 4% rule—it’s everywhere.

But blindly using it is one of the riskiest moves you can make for two reasons.

First, it’s overly conservative and can lead to dramatically underspending over a 30-year retirement.

In fact, historically, retirees using the 4% rule were more likely to end retirement with 5x their initial nest egg than to have less than they started with.

In other words, this outdated rule can prevent you from enjoying the money you worked so hard to save.

On the other end of the spectrum, fixed 4% withdrawals can backfire if sequence risk rears its ugly head.

Sequence risk is the danger of experiencing poor investment returns in the early years of retirement.

If markets fall early and you keep withdrawing the same fixed amount, you’re locking in investment losses.

And this is why retirees with identical portfolios can have dramatically different outcomes, just based on when they start withdrawing.

A better approach to retirement income is a flexible withdrawal strategy, like Guardrails.

With Guardrails, you begin retirement with a higher withdrawal rate—typically 5-6%—allowing you to enjoy your early, active years.

And to ensure you don’t overspend and outlive your money, you establish a withdrawal range.

In short, when markets go up, the rules allow you to withdraw and spend more. When markets go down, you’ll temporarily need to withdraw a little less.

This flexible approach helps you maximize retirement spending while mitigating the chances of running out of money.

Pitfall #4: Overlooking the Rest of the World

Here’s the deal – from 2000-2009, the S&P 500 returned negative 9%, with dividends reinvested.

A full decade of no growth.

If you’re still working and regularly stashing money away for retirement, an event like this isn’t catastrophic.

But let’s say you happened to retire in the year 2000, right when this “lost decade” began.

Let’s also say you had a $1 million nest egg invested in a low-cost S&P 500 fund and began withdrawing 5% per year adjusted for inflation. In just 16 years, you would have run out of money.

On the other hand, a globally diversified investor taking the same 5% withdrawals would have ended that same 16-year period with more money than they started with.

Investing in large, U.S.-based companies might feel safe because the names are familiar and it’s your home country.

But putting all of your eggs in one basket—especially in retirement when you are living off your portfolio—can be a recipe for disaster.

So, if you’re in retirement or close to it, consider global diversification to help support sustainable withdrawals and mitigate the chances of running out of money.

Pitfall #5: The Tax Planning Gap

Unfortunately, taxes don’t end in retirement. In fact, they typically get more complicated.

When Required Minimum Distributions (RMDs) collide with other retirement income sources like Social Security, pensions, dividends and interest, and more, you can find yourself in a higher tax bracket than when you were working.

And that higher tax bracket can trigger additional unwanted taxes, like Medicare IRMAA. It can also spike the taxes you pay on Social Security income.

And once those tax surprises hit, it may be too late to do anything about them.

That’s why proactive tax planning in your late 50s and 60s can be so powerful.

For example, partial Roth conversions before age 73 can help reduce future RMDs, avoid phantom taxes like IRMAA, and even lower your lifetime tax bill.

If, like most people, you don’t like paying taxes on Roth conversions, consider pairing them with a donor-advised fund contribution to offset the taxes while supporting causes you care about.

Lastly, properly coordinating withdrawals across all account types (taxable, tax-deferred, and tax-free) is also key to helping you manage the tax gap in retirement and ensures you’re not tipping the IRS along the way.

Pitfall #6: The Cash Management Mistake

I get it, cash feels safe.

But too much of it—especially in retirement—can quietly erode your financial future.

Even in today’s higher-rate environment, cash typically fails to keep up with inflation.

Worse, many retirees often panic and move in and out of cash during stock market volatility, locking in losses and missing recoveries.

I’ve seen retirees make the opposite mistake, too—holding too little cash and being forced to sell investments during a market downturn to cover living expenses.

A scenario like that can create real, permanent damage.

So, what’s the solution?

One approach is a simple, tiered system for managing your nest egg:

- 6 months of cash set aside for unknown expenses (i.e., emergencies)

- 12 months of cash for known expenses (gas, groceries, upcoming tax bill, etc.)

- 2-5 years of living expenses invested in high-quality bonds

- The remainder to be invested in a diversified, global stock portfolio

A system like this provides confidence and flexibility to handle market surprises without derailing your plan.

Yes, to some, it might seem too conservative. But, remember, the goal is not to chase returns with short-term money—it’s to protect your long-term money from short-term decisions.

Pitfall #7: The Long-Term Care Illusion

We’ve all heard the stat: 70% of people over age 65 will need some form of long-term care before the end of life.

That statistic is true. But here’s what you rarely hear:

Only about 13% of today’s 65-year-olds will spend more than $150,000 out-of-pocket on long-term care.

And roughly 63% will spend nothing.

That changes the conversation.

Yes, long-term care is still a risk. But it’s not an automatic catastrophe for most people.

So instead of reacting out of fear and buying an expensive insurance policy—or avoiding the topic altogether—build a plan that aligns with your needs and your goals.

That could mean earmarking part of your portfolio to self-fund this potential, future expense.

It could mean doing a TAX-FREE exchange from an old insurance policy you don’t need into a new policy that provides long-term care protection.

Or it might mean adjusting your spending so you can confidently absorb an expense like this if it occurs.

What matters is that your plan is intentional.

Because long-term care affects everything—from when you retire to how much risk you take to what you leave behind.

The Underlying Problem: Treating Retirement Like a Math Problem

When you look at these seven pitfalls together, you’ll notice that they all stem from a single problem: treating retirement like a math problem instead of a dynamic, decades-long transition.

In the accumulation years, your job was simple: Save. Invest. Repeat.

In retirement? You need a process. One that coordinates taxes, investments, insurance, and income.

And they all need to work together, not in isolation.

The process we implement for our clients is called the Total Retirement System™.

Here’s how it works and how you can use it to ensure you never have to un-retire.

Introducing the Total Retirement System™

Step 1: Tax Planning

You’ll begin this step by running a long-term tax analysis. Ultimately, this exercise helps you compare your current tax rate to your future projected rate—and decide when and how to make tax-smart moves in retirement.

Moves like Roth conversions during low-income years. Harvesting capital gains. And drawing from the right accounts at the right time.

This foundation directly informs step two—developing your tax-efficient income plan. Or, what I refer to as your Retirement Paycheck.

Step 2: Income Planning (Your Retirement Paycheck)

Forget rigid rules like the 4% rule.

Instead, consider a more flexible Guardrails strategy. This lets you confidently spend more money in retirement by adjusting withdrawals up and down based on different market environments.

The Guardrails strategy also helps you establish and maintain a proper cash reserve, so you’re not forced to sell investments during downturns.

Step 3: Legacy Planning

If you have goals like leaving money to heirs or giving money to charity, it’s important that they are documented and integrated into the plan.

This is also where you’ll identify and create a plan for potential risks like long-term care or estate taxes upon death, and ensure your estate documents are properly aligned with your intentions.

Step 4: Investments

With a comprehensive plan in place, it’s time to align your investments with your documented needs, goals, and wishes.

(And by the way, this is completely backward from how most people approach investing. Most people start with choosing an investment strategy and then go through a planning process to see if they can retire. But that would be like taking a prescription before getting a diagnosis and recommendation from a doctor. So, Investments as the final step in the Total Retirement System™ are very intentional. We want the plan to influence the investment strategy, not the other way around.)

Aligning your investments with your documented needs and goals includes diversifying globally, choosing bonds that offer real protection, and aligning your asset allocation with your risk tolerance and time horizon.

It also includes understanding your risk capacity. I.e., how much risk you NEED to take with your investments to reach your stated goals. Perhaps your plan validates that you can take less risk than you thought, helping you sleep better at night, and avoiding having to worry about daily headlines. On the other hand, sometimes the risk capacity exercise results in having to take more investment risk to meet the documented goals of the plan. In those situations, you can either accept additional market risk or, if possible and desired, adjust your goals downward. For example, you might downsize your home or find ways to cut spending so you aren’t forced to take more risk than you are comfortable with.

Conclusion: Building a Flexible Plan That Lasts

When you put all of this together, you get a retirement system that adapts with you, not just today, but as life and markets change.

Because staying retired isn’t just about hitting a savings number or following a simple rule of thumb.

It’s about having a flexible plan that can adjust with your life, goals, and whatever the future throws your way.

If you don’t have a plan or you’re concerned about your retirement sustainability, and you would like professional help, consider reaching out to my team. We specialize in helping people who are retired or close to it reduce taxes, create a reliable retirement paycheck, and make work optional. We offer a Free Retirement Assessment, answering your big questions and showing you exactly how we can help, so you can make an informed decision about hiring us. Click the link in the episode description to learn more or visit freeretirementassessment.com.

Thank you for listening, and once again, to view the research and articles supporting today’s episode, just head over to youstaywealthy.com/242.

Disclaimer

This podcast is for informational and entertainment purposes only, and should not be relied upon as a basis for investment decisions. This podcast is not engaged in rendering legal, financial, or other professional services.