Annuities are often sold as a simple solution to a complicated retirement problem.

Guaranteed income. Protection from market volatility. Peace of mind that your money won’t run out.

But behind those promises is a much more complex set of trade-offs that many investors don’t consider.

Because while annuities can play a role in retirement planning, evaluating them in isolation often leads to unintended consequences (higher fees, reduced flexibility, extra taxes).

So in today’s episode, I break down how annuities actually work.

We’ll walk through the major types of annuities, how “guarantees” are structured, what you’re really paying for, and where the risks tend to show up later in retirement.

I’ll also explain when annuities may make sense, when they don’t, and how to evaluate them as part of a coordinated retirement plan so you can make informed decisions with confidence.

Listen To This Episode On:

When You’re Ready, Here Are 3 Ways I Can Help You:

- Schedule a Free Retirement Strategy Session. Get your questions answered + learn how we can help you improve retirement success and lower taxes.

- Listen to the Stay Wealthy Retirement Show. An Apple Top 50 investing podcast.

- Join My Retirement Newsletter. Weekly retirement and investing tips (delivered to our inbox!)

+ Episode Charts

+ Episode Resources

+ Episode Transcript

Retirement planning asks you to solve a problem. No one ever solved while working, funding an unknown length of time with a finite pool of savings, we don’t get to know how long retirement will last. What we do know is that for many people retiring today, it’s much longer than previous generations.

Living into your late eighties or nineties is no longer unusual, especially if you’re healthy and longevity runs in your family. Stretch that timeline out far enough and a few things become unavoidable. Markets will be volatile. Inflation will raise the cost of living year after year, and some of the biggest expenses, particularly healthcare, tend to arrive later when adjusting becomes harder.

That uncertainty is what annuities are designed to address. They promise stability in an environment that feels anything but stable, predictable income, less worry about the markets protection against outliving your money, and that promise resonates for a reason.

But what often gets lost is how those guarantees actually work, what they truly protect and the trade-offs required to get them.

So in today’s episode, I’m breaking it all down. I’m sharing how annuities actually work, why they’re sold the way they are, and how to think clearly about whether an annuity improves your retirement plan or simply trades flexibility and long-term purchasing power for the comfort of certainty.

Welcome to another episode of the Stay Wealthy Retirement Show. I’m your host Taylor Schulte, and every week I tackle the most important financial topics to help you stay wealthy in retirement. And now onto the episode.

Annuities Explained: When Guarantees Help—and When They Hurt Your Retirement

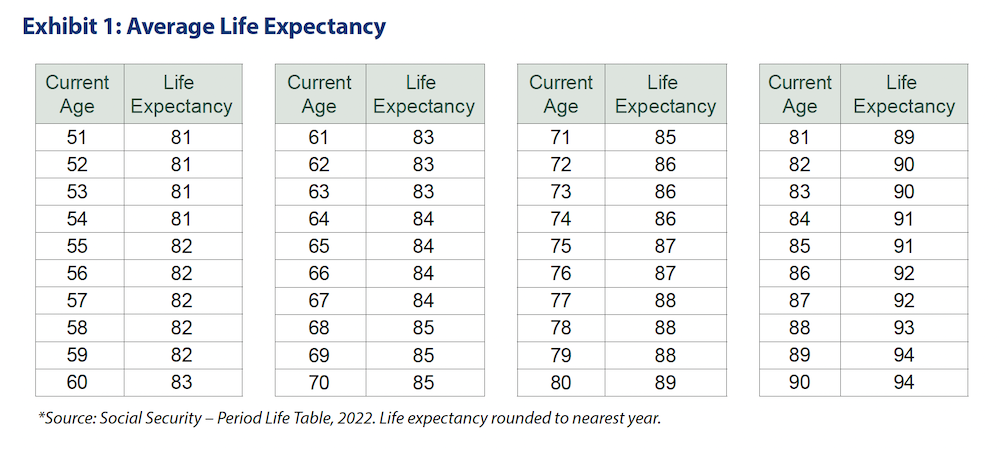

Retiring today is different than it was even a few decades ago. Most people should expect to live a much longer, more active life in retirement than their parents or grandparents. According to Social Security data, a 65-year-old today has an average life expectancy of 84, but that’s just the average.

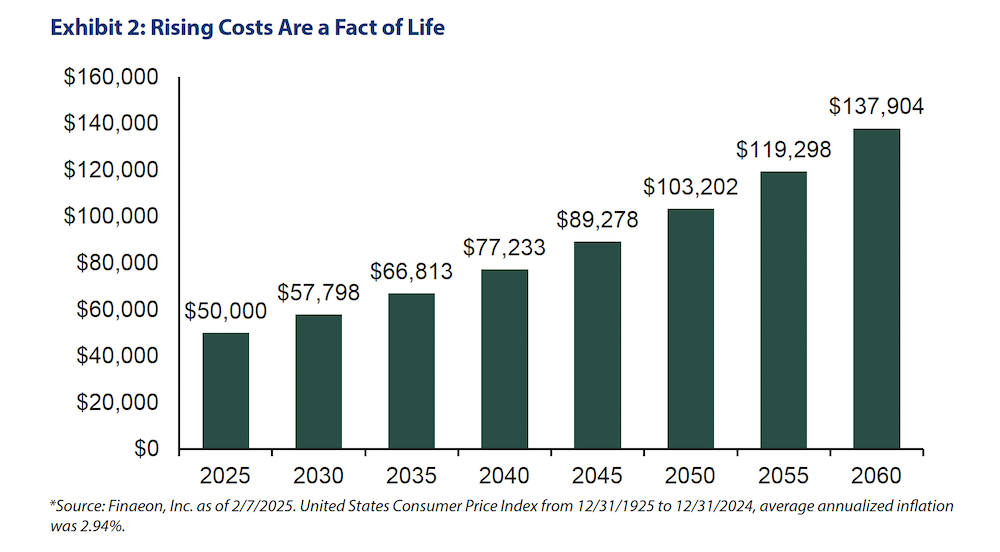

If you’re in good health and have a family history of longevity, you may need to add more years to your planning horizon. This creates what’s called longevity risk, the possibility that your portfolio may not be able to provide for you over a 25 or 30-plus-year retirement. And here’s where it gets even more challenging. Inflation doesn’t stop just because you’ve retired since 1925, inflation has averaged about 3% per year.

If that continues, someone who needs $50,000 annually to cover living expenses today would need nearly $120,000 30 years from now just to maintain the same purchasing power. And by the way, medical expenses, which tend to be the largest, most unpredictable expense for retirees, have increased by about 6% per year. Double the rate of headline inflation. These fears outliving your money, inflation eroding your purchasing power. Market volatility are exactly what annuity salespeople tap into, and I get it.

The promise of guaranteed lifetime income sounds like the perfect solution, but as I’m about to show you, that guarantee comes at a cost. A cost that typically outweighs the value these policies deliver at a high level. There are two broad categories of annuities, deferred annuities, and immediate annuities.

A simple way to think about a deferred annuity is like a traditional IRA wrapped inside an insurance product. You contribute money to the policy, the funds are invested and grow tax deferred over time, and then at a later date, you convert that balance into a stream of guaranteed income payments. Immediate annuities often called single premium immediate annuities or SPIAs work very differently.

With a SPIA, you’re not deferring or growing money inside the product. Instead, you give the insurance company a single lump sum of money, let’s say $100,000 and in return, that lump sum is immediately converted into a guaranteed stream of income either for a specific number of years or for the rest of your life.

You get to choose what best fits your needs. But one important thing to understand is that the longer the guaranteed payment period is, the lower your monthly income will be, and that’s because from the insurance company’s perspective, a longer payout horizon means more risk and that risk needs to get priced into the policy terms.

Now, one of the biggest advantages of SPS is their simplicity. They’re generally easy to understand with fewer moving parts, fewer confusing guarantees, and far less fine print to sort through than many other annuity and insurance products. That said, SPIA are still financial products and like all financial products, they aren’t a good fit for everyone.

Beyond fees, the bigger issue might be the opportunity cost. When you purchase a spia, you give up control of a lump sum in exchange for guaranteed income instead of keeping those assets invested and building income for yourself, often with more flexibility and the ability to leave money behind because of this trade-off, we rarely consider SPIAs for our clients when we do.

It’s typically much later in retirement, often around age 80 and for very specific purposes. In those cases, a SPIA is used to fund known non-negotiable expenses while directly addressing longevity risk, for example, consider an 80-year-old client in good health with $2 million through planning, we determine that $1 million is sufficient to fund the remainder of their estimated lifetime spending while the other $1 million is earmarked for errors.

If the client does not want investment risk on the $1 million needed for expenses, is fully comfortable spending all of it during their lifetime and wants to protect against outliving that portion of their assets, well, one option is to allocate that specific bucket, that $1 million to a SPIA in return. The insurance company provides guaranteed income for life regardless of how long the client lives.

Now, the downside is obvious and it’s an important one. If this person in this example buys a SPIA and passes away shortly after, whether it’s the next day, the next month, or even a few years later, that $1 million is gone, the insurance company has that money.

So in that scenario, you would’ve been far better off keeping the money invested and following a disciplined withdrawal strategy on your own, knowing that whatever wasn’t spent could support other goals like charitable giving or inheritance for children or even grandchildren. That’s the core trade-off with SPIAs certainty and longevity protection on one hand versus flexibility control and legacy potential on the other.

So now that we understand the difference between deferred and immediate annuities, what exactly is a variable annuity? While there are some unique exceptions for the purpose of today’s conversation, a variable annuity is a type of deferred annuity. The simplest way to think about this is this, take a diversified portfolio of mutual funds, add in tax-deferred growth, and then wrap it all up inside an insurance contract. That structure in essence, is a variable annuity.

That’s pretty much it. Those are the three parts that make up a variable annuity.

One, a basket of mutual funds, two, a tax benefit and three various types of insurance through the form of guarantees or riders. The diversified portfolio of mutual funds is pretty simple to understand. Those don’t look really any different than what you would find in your workplace 401k, just a plain old list of stock and bond mutual funds to choose from. And just like a 401k, the performance of the underlying funds you choose determines the growth of your annuities contract value.

What’s not so easy to understand is the insurance policy that wraps all this up and turns it into a variable annuity. But really quick before we get there, there’s one major pitfall that I want you to watch out for. When you put money in a variable annuity, you have the option to fund it with pre-tax IRA dollars or with after-tax dollars like money in your brokerage account or even your checking or savings account at the bank.

Now, I just told you a minute ago that a variable annuity is a tax-deferred savings vehicle. A traditional IRA is also a tax-deferred savings vehicle. Therefore, in most cases, there really isn’t a compelling reason to invest traditional IRA dollars into a variable annuity. You’re paying extra fees to get a tax benefit that you essentially already have functionally you’re putting a tax-deferred account inside of a tax-deferred account.

Now while it’s not something I would likely advocate for, there can be situations where the insurance features of a variable annuity like certain income guarantees or death benefits are what someone is really after, and that might be the reason it ends up inside of an IRA, but I want it to be crystal clear that you’re paying for those insurance features as well as the extra tax deferral that you don’t need because you already have it.

So that’s what I want to focus the rest of this episode on the insurance policy and the benefits so that you can make an educated and informed decision to keep things simple.

There are two important things you need to understand about the insurance component of a traditional variable annuity. Things that are easy to miss if you’re not paying close attention.

Number one, the guarantees. Guarantees are a big selling point in the variable annuity world, and there are two common ones you’ll often hear about.

First, a guaranteed rate of return. The salesperson may explain that your annuity is guaranteed to grow by let’s say 6% or 7% per year no matter what the market does.

Second locked in gains. If your account reaches a new high, you might be told that that higher level is now locked in and can never go below that amount even if the market tanks.

These guarantees if they exist in the contract are not lies. But there’s a critical misunderstanding that trips people up and that is that these guarantees don’t apply to the actual money you can walk away with. They apply to a separate number inside the contract, often called the income benefit base.

Here’s the simplest way I can explain it. The income benefit base is an accounting figure that the insurance company uses to calculate how much income they’ll pay you. If you keep the contract and use it for lifetime withdrawals down the road, it is not a pile of money that you can go and cash out.

So when a salesperson says that your annuity is guaranteed to grow at 7%, what they really mean is that this internal accounting number grows at 7%, not your actual account value, your actual account value, the money you can walk away with if you terminate, the policy still rises and falls with the market just like any other investment.

Here’s what that looks like in practice. Suppose you invest $100,000 into a variable annuity with these guarantees, the market declines and the investments inside the annuity are now worth $80,000. Well, if you decide that the product is no longer for you and you want to get out, you would walk away with $80,000 minus any surrender charges that guaranteed 7% growth on the income benefit base doesn’t change that from a pure market risk standpoint, that’s no different than owning similar funds outside of the variable annuity.

The annuity wrapper doesn’t magically make your investments less risky or less volatile. So what’s the actual insurance here? The real protection kicks in later if you keep the contract for a long period of time and start taking guaranteed income withdrawals to help fund retirement expenses. If poor market performance or your longevity eventually drives your actual account value down to zero, the insurance company keeps paying your guaranteed income for life.

That’s where their risk shows up and that’s the benefit that you’re paying for. It’s not fake, but it’s not a guaranteed return on your money that you can access. It’s a promise about how income is calculated and paid in the future, not a promise about your account balance today.

When in doubt, ask the insurance company or agent one simple question. If I cancel this contract in one year, three years, five years, or even 10 years, how much can I actually walk away with after fees and after taxes? Get clear answers to that and you’ll learn a lot about what you’re actually buying and whether those guarantees are worth the cost. Speaking of costs, that’s the second thing that I want to touch on regarding the insurance component of these variable annuities. As mentioned, variable annuities are insurance policies and buying insurance. As you guys all know, costs money.

Every single guarantee, every benefit that you might see attached to a variable annuity is something that you are going to be paying for. Nobody’s giving you all these great bells and whistles, downside protection, inflation protection, guaranteed rates or returns, guaranteed income for life. Nobody is giving away these benefits for free. Any benefit that you see on an advertisement or that somebody is telling you about, just remind yourself that you are paying for it.

The insurance company has priced this into all of their products and they know on average across millions of policies that they are going to come out ahead by a wide margin over a long period of time. Here are just a few of the fees that you could be paying for if you open up your variable annuity and look under the hood. Mortality and expense risk fee, administrative fee, annual contract fee, advisor fee, mutual fund expense fee, surrender fee, rider fees, and there could be dozens of rider fees.

According to an analysis of over 48,000 unique annuity policies between 2020 and 2024, these fees can total as much as 3.88% per year and taking nearly 4% in fees from the contract every single year will absolutely eat away at the value of your invested dollars over time and reduce the insurance and income guarantees.

We recently met with a new client who had $1 million invested in a variable annuity that was costing them close to that 3% number or roughly $30,000 per year. And to make matters worse, that $1 million was invested using traditional IRA dollars a tax-deferred account inside of a tax-deferred account paying $30,000 per year for insurance guarantees that they didn’t need without any comprehensive wealth management or planning services.

This policy specifically was sold to them in 2021 not too long after the COVID crash, when everyone was panicked and it was positioned as this low risk investment option, but that’s not what it was, and it most certainly was not what they needed, and although she knows that now, it’s not as simple as just canceling the policy, cashing out and moving on, and that’s because there’s another layer of common fees charged by variable annuities known as surrender fees.

A common surrender fee schedule starts at 7% of the premium and declines to zero over time, often taking seven to 10 years to fully expire. Let’s put that in real dollars here. On a $1 million annuity, a 7% surrender fee means you’re paying $70,000 just to get out of the contract in year one. Even in year four, you might still be looking at $40,000 or more just to get out. That matters because surrender fees don’t just restrict access to the money.

They lock you into the assumptions baked into the contract at the time of sale, the income structure, the guarantees, the limited investment menu, and just like our client experienced, many variable annuities are sold during periods of stress. After a market drop or during a period of economic uncertainty, the surrender period then stretches across years. When circumstances tend to change, the economy improves spending patterns evolve.

Tax law is overhauled. Health changes goals shift. So even when someone realizes the product no longer fits, it’s possible that the cost of exiting forces them to delay taking action and keep in mind, while surrender fees eventually expire, the design of the annuity does not reset. The original contract still governs how income is calculated, how increases happen, and when adjustments are allowed.

Those features matter more the longer the policy is held, which brings us to a risk that grows with time and that is inflation. Inflation affects every retirement income strategy, but it plays a specific role in variable annuities. Even though variable annuities are invested in stocks and bonds through the mutual fund sub-accounts that we previously discussed, the income and withdrawal guarantees themselves are usually fixed in nominal dollars. So if markets underperform and you fall back on the guarantee, you are then locked into a flat payment that inflation will slowly chew apart.

In other words, variable annuities are designed to help you not run out of money, but they’re not automatically designed to help you keep up with rising prices. Of course, the annuity company will happily sell you a cost of living benefit or inflation rider that promises to adjust your income each year when you begin taking withdrawals. But every feature you add to the policy comes with higher expenses, which ultimately reduces your income payment. It’s a catch 22.

So if variable annuities contain high fees, limit your flexibility, increase inflation risk, and provide insurance guarantees that you may not need, what is the alternative? The alternative is to simply build your own annuity. In other words, the alternative is to construct an invest in a globally diversified portfolio of stocks and bonds and apply a flexible withdrawal strategy like guardrails or floor and ceiling to create an attractive income stream that you can’t outlive.

Keep in mind, in addition to your allocation to high-quality bonds, a good flexible withdrawal strategy will also mandate a healthy allocation to cash somewhere between five and 10% depending on your situation. So while you don’t have insurance guarantees to protect you from market downturns, you do or you should have a war chest of cash and bonds to supplement your income and prevent you from needing to sell stocks at lower prices.

And even if you need to hire a financial advisor to help implement this, you’ll still be paying a fraction of the fees charged by typical insurance companies, and you’re likely going to receive additional wealth management services as well, like tax planning, estate planning, long-term care planning, and more in addition to lower fees, more flexibility and reduced inflation risk. Skipping the annuity and creating your own retirement income plan helps you avoid overpaying the IRS.

One of the additional drawbacks with variable annuities that we haven’t discussed yet is how they are taxed when you finally begin taking withdrawals, especially compared to owning investments in a plain vanilla regular brokerage account. Let’s start with non-qualified variable annuities, meaning variable annuities funded with after-tax dollars from your brokerage account checking or even savings account.

When you withdraw money from a non-qualified variable annuity, any investment gains are taxed as ordinary income, not at long-term capital gains rates, not at qualified dividend rates, ordinary income, which for most people is the highest tax rate they’ll pay, but it gets worse.

The IRS requires what’s called life or treatment or last in first out. That means investment gains come out first. Every dollar you withdraw up to the amount of your total earnings is taxed as ordinary income before you ever touch your original principle. Now, compare that to a taxable brokerage account.

Investments held longer than one year are taxed at long-term capital gains rates, which range from 0% to 20% depending on your income. Qualified dividends receive the same preferential treatment. You control what you sell when you sell it and how income shows up on your tax return. You can harvest losses to offset gains and manage your tax bill over time instead of letting it manage you.

That flexibility simply does not exist inside a variable annuity. Once money goes in, growth is tax deferred, but every dollar of that growth that comes out is taxed as ordinary income. And if you access a non-qualified annuity before age 59 and a half, the IRS adds a 10% penalty on the earnings portion. Similar to an early IRA withdrawal, if the annuity is purchased with pre-tax IRA money, the tax picture is even simpler. Every dollar you withdraw is tax as ordinary income just like any other IRA distribution.

The annuity has not improved your tax outcome at all. You’ve just wrapped higher cost insurance features around dollars that were already going to be fully taxable. So when you compare a variable annuity to a plain vanilla brokerage account holding low cost index funds, here’s what you’re giving up.

Lower long-term capital gains and qualified dividend tax rates control over the timing and character of taxable income and the ability to harvest gains and losses and manage taxes year by year. That’s a meaningful trade-off and one that deserves careful consideration before signing anything.

Now, most of what I’ve discussed so far applies to what I’d refer to as traditional variable annuities. If an annuity is being marketed with guarantees, downside protection, or reduced market risk, you’re almost certainly looking at one of these traditional products that tend to be more expensive, complex, and bundled with insurance features that many people don’t really need.

That said, it’s worth noting that there are a wide variety of low cost no frills variable annuities that don’t get as much attention but do exist in the marketplace. For example, fidelity offers what they call the Fidelity personal retirement annuity, which costs roughly 0.1% to 0.25% per year and has no surrender charges with these plain vanilla stripped down annuities, you essentially get the benefits of tax deferral, but none of the insurance guarantees that we’ve spoken about today, it’s essentially another retirement savings vehicle for those who have maxed out all other tax advantage accounts and want to save additional dollars for retirement on a tax deferred basis.

But this is where the trade-off matters, because while the fees are low and the growth is tax deferred, you have to remember that future withdrawals on the growth are taxed as ordinary income. Unlike a taxable brokerage account where long-term capital gains and qualified dividends receive preferential tax treatment, every dollar of annuity earnings eventually comes out at ordinary income tax rates.

So the real question becomes, does the benefit of tax deferral outweigh the higher tax rate you’ll pay later? In my experience, it usually doesn’t. I found that for most investors, it’s more effective to buy and hold low-cost, low-dividend ETFs in a taxable brokerage account and manage capital gains deliberately over time rather than wrapping those dollars inside a variable annuity.

However, there is one specific use case where I do like these low-cost annuities and it involves money that’s already trapped inside another insurance product.

Let me give you a real example. One of our clients, Tim, was sold a whole life insurance policy 15 years ago that he really didn’t need. The policy had accumulated significant gains, and so if we had surrendered it, those gains would’ve been taxed immediately as ordinary income At the time Tim was in his peak earning years and adding more taxable income to the picture just didn’t make sense.

So instead, we recommended that he do a 10 35 exchange, which at a high level allows for a tax-free transfer between like kind insurance products. Specifically for him, we recommended that he exchange this whole life policy into the ultralow cost variable annuity product at Fidelity.

Doing this allowed him to exit the expensive whole life policy that he didn’t need, defer the taxes on the embedded gains, and continue growing the money in a tax lower cost, more flexible structure. The plan was to eventually liquidate the Fidelity annuity during his lower income retirement years when his tax rate would be meaningfully lower.

But more recently, Tim decided that he wanted to explore long-term care coverage, not because he really needed it, but just for some extra peace of mind. Well, what he didn’t realize is that the low cost fidelity annuity that he exchanged into gives him the flexibility to execute another tax-free exchange into a hybrid long-term care policy, which we’re currently evaluating.

So while these low cost no surrender variable annuity products might not always be great savings vehicles in some unique situations, they can be great planning tools. Really quick before we move on, two important notes here.

1.) First, low cost no frills. Variable annuities typically do not have any surrender charges, which is what makes this kind of planning flexible. But if an annuity does have surrender fees, just know that a 10 35 exchange does not eliminate them. Always understand the contract before initiating any exchanges.

2.) Second, fee only firms like ours don’t earn commissions on insurance products. We recommended this exchange to Tim because it was in his best interest and aligned with his long-term needs and goals, not because we were paid to do it. If you work with an advisor who earns commissions, that doesn’t automatically make their recommendations wrong, but it does mean conflicts of interest should be considered and discussed before signing on the dotted line.

Okay, before we wrap up today, I want to briefly address fixed annuities since some of you may have been wondering how they fit into today’s discussion. While some fixed annuities are immediate, most are structured as deferred products, and without going too deep, many of the same drawbacks we’ve discussed with variable annuities apply here as well. High internal costs, surrender charges, complicated guarantees, and fixed payments that typically do not adjust for inflation.

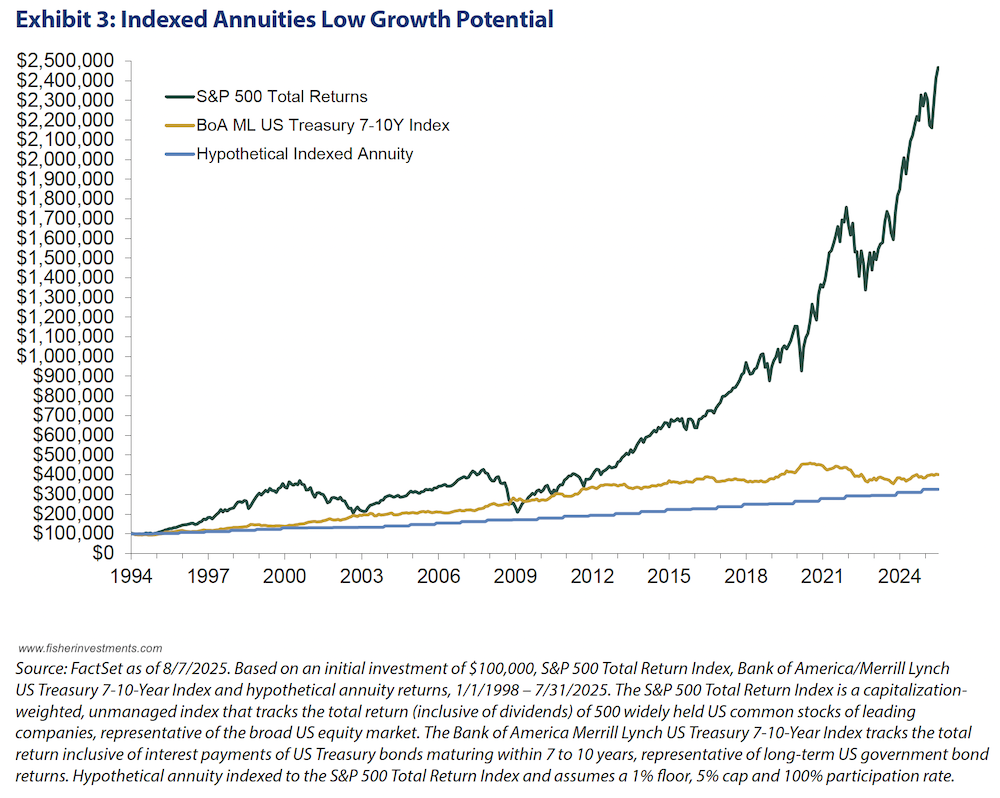

But the biggest issue of fixed annuities, especially fixed indexed annuities, is opportunity cost. With these products, your return is tied to a market index like the s and p 500, but in exchange for downside protection, your upside participation in the index’s performance is capped. That downside protection can sound comforting, but over long periods of time, the trade-off typically isn’t worth it.

For example, from January, 1994 through August of 2025, a $100,000 investment in a simple 60% US stock, 40% bond portfolio would’ve grown to roughly $1.2 million.

In contrast, the same $100,000 invested in the hypothetical fixed indexed annuity measured in this study grew to only about $325,000. As we discussed earlier, inflation has averaged around 3% historically. So when you cap upside over long stretches of time, you dramatically increase the risk of losing purchasing power in retirement, and that’s why retirement investors should be cautious about trading long-term growth for the illusion of safety.

To round out today’s episode and help you take action, here are some key questions you should be able to answer about any annuity you own or you’re considering. What type of annuity is it? Deferred, variable, fixed, immediate indexed? What does the annuity cost each year, both in fees and missed opportunities? Is there a charge for withdrawing assets early from your annuity? Are there performance caps or market participation rates? Is the guaranteed income stream adjusted for inflation each year?

What are the trade-offs incurred by owning your annuity? If you’re unsure about any of these details, you’ll likely want to get clear answers to these questions and more before you make any final decisions or contribute more money.

If today’s episode reinforced how interconnected planning decisions really are and why insurance or investment products cannot be evaluated in isolation, this is exactly the type of work my team and I do every single day.

We specialize in helping retirement savers over 50, coordinate every major decision, tax planning, income strategy, investments, healthcare, and legacy into one clear integrated system, so nothing is working against anything else. That’s especially important when evaluating complex products like annuities, where a single decision can ripple across your entire retirement plan for decades.

So if you’re nearing retirement or already there and you want a second pair of eyes on your portfolio and retirement plan, we’d be honored to have a conversation to see if there’s a good mutual fit. You can learn more and schedule a free retirement strategy session through the link in the episode description or by visiting definefinancial.com and clicking get started.

Thank you as always for listening and to view the research and resources referenced in today’s episode. Just head over to youstaywealthy.com/269.

Disclaimer

This podcast is for informational and entertainment purposes only, and should not be relied upon as a basis for investment decisions. This podcast is not engaged in rendering legal, financial, or other professional services.