Today I’m continuing our multi-part series on Dividend Investing.

Specifically, in part two, I’m sharing:

- What the long-term performance has been for dividend-focused funds

- Why popular dividend investing charts can be incomplete (or misleading)

- The 3 primary reasons dividend strategies typically underperform

If you want to learn more about dividend investing and why it may not be the magical solution it’s often marketed as, you’ll enjoy this episode.

(Missed Part One? Click here to get caught up.)

Listen To This Episode On:

When You’re Ready, Here Are 3 Ways I Can Help You:

- Get Your FREE Retirement & Tax Analysis. Learn how to improve retirement success + lower taxes.

- Listen to the Stay Wealthy Retirement Show. An Apple Top 50 investing podcast.

- Join My Retirement Newsletter. Weekly retirement and investing tips (delivered to our inbox!)

+ Episode Resources

+ Episode Charts

+ Episode Transcript

Taylor Schulte: Welcome to the Stay Wealthy podcast, I’m your host Taylor Schulte, and today I’m sharing part two of our multi-part series on dividend investing.

Specifically in today’s episode, I’m discussing the long-term historical performance of dividend-focused strategies.

I’m also sharing three reasons why dividend investing, historically, has failed to outperform other major asset classes.

To grab the links and resources mentioned in this episode, just head over to youstaywealthy.com/218.

Dividend Investing (Part 2): Three Reasons Why Dividend Strategies Underperform

As shared in part one, the majority of publicly traded companies in the U.S. pay a regular dividend. If an investor spends the dividends they receive, the total value of their portfolio will be smaller as a result. If the dividends are automatically reinvested, the total value of the investor’s portfolio will remain unchanged on the day the dividend is paid – and that’s because the price of the stock or fund will typically be reduced by the amount of the dividend.

If we simply compare spending the dividends you receive versus reinvesting them back into your portfolio, it should hopefully be clear that reinvesting them will, of course, lead to more money in your pocket. If I don’t eat a slice of birthday cake, I’ll have more cake. If you don’t spend your dividends, you’ll have more money.

To be extra clear, I’m not saying that high-yielding dividend stocks or funds lead to superior investment returns. In fact, historically, we’ve seen the opposite. Dividend-focused stocks or funds, over long periods of time, have not produced the outperformance that many investors are led to believe.

And today I’m going to explain why that is. Specifically, I’m going to share three main reasons why dividend-focused strategies have underperformed.

But before I share them and explain the “why”, let’s start with the “what” – what has the performance been, historically, for this very popular asset class?

To start, let’s first look at some actual, real-life dividend-focused funds open and available to all investors. In other words, instead of looking at indexes that can’t be invested in, let’s examine the actual dividend strategies you could have invested in for the last 30 years. And in case you’re wondering, the reason we can only go back 30 years is that there aren’t many dividend-focused funds with long track records that are still in existence today.

Hundreds (maybe thousands?) of them have closed or merged over the last three decades – and while there are valid reasons for closing or merging a fund, it’s usually a result of poor performance, lack of investor interest, and in turn, too few assets to support the ongoing operating expenses.

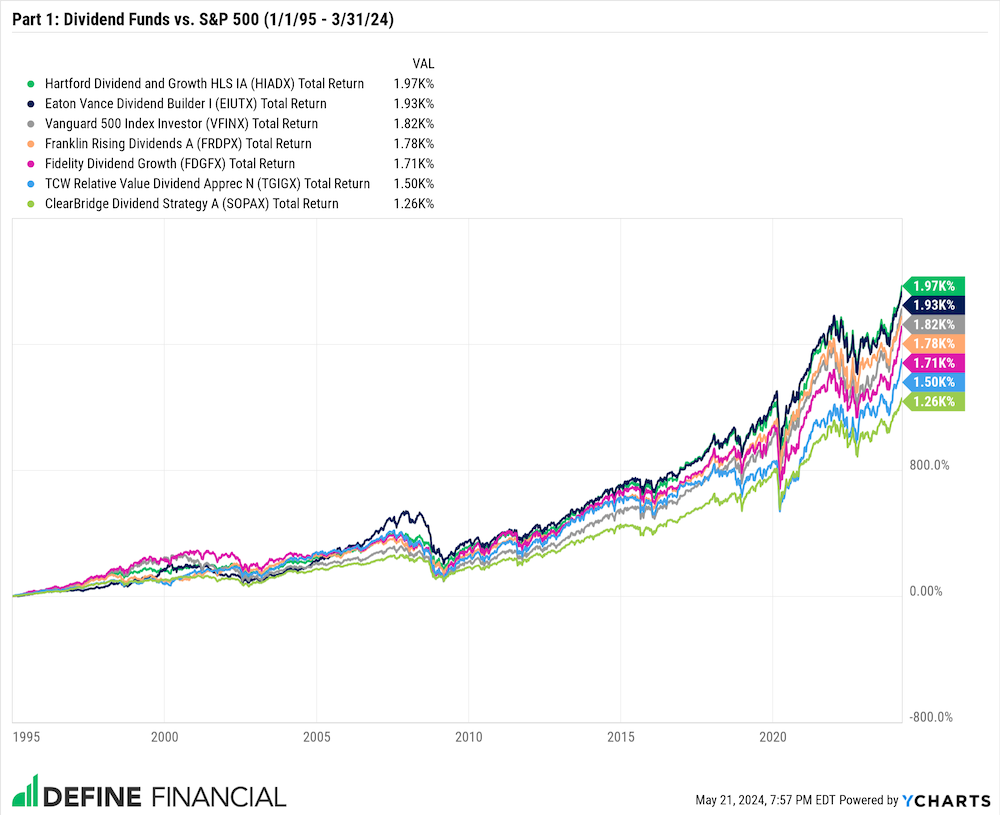

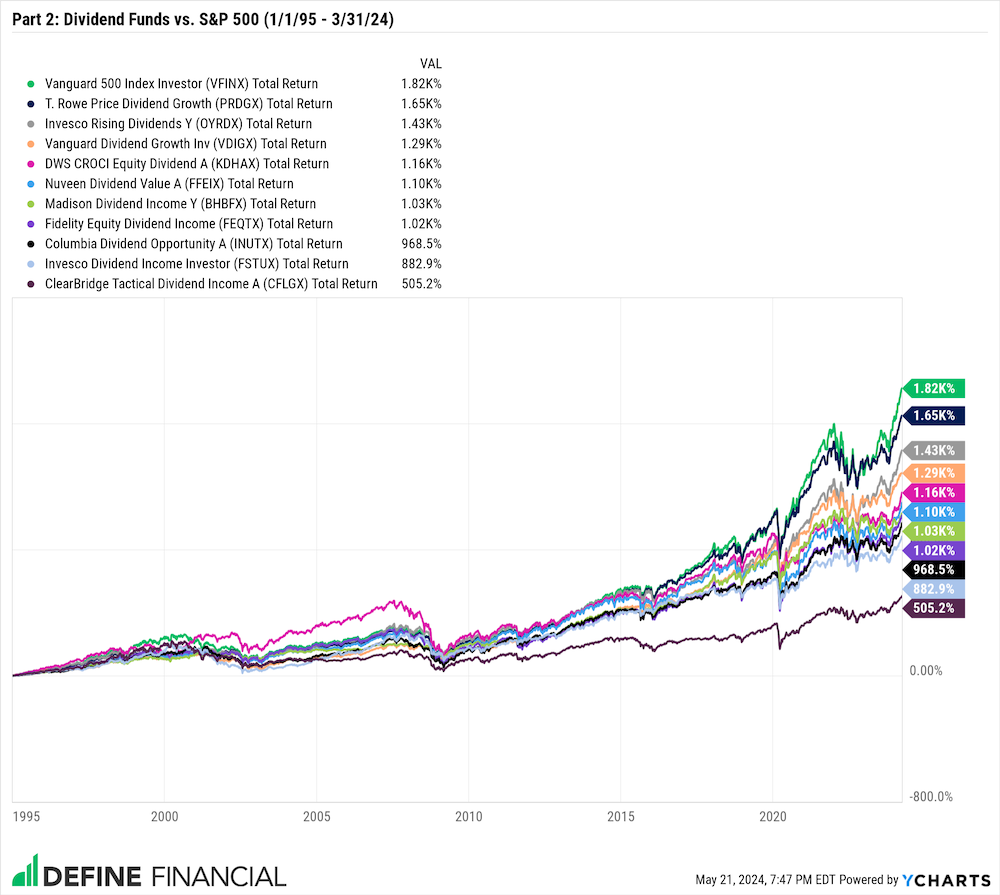

So, to give us a decent enough sample size, I went back to January 1st, 1995, where there are a total of 17 open-ended dividend-focused funds that are still in existence today. Of those 17 funds, 15 of them (or 88% of them) underperformed the Vanguard S&P 500 Fund through March 31st of 2024.

Yes, that does mean that two of the funds did outperform, but hopefully, we’re all in agreement that unless you had a perfectly working crystal ball, it would have been impossible to pick the two funds out of 17 that would happen to outperform the S&P 500 over the last 30 years.

And just so you don’t think I’m only picking on old-school, high-cost actively managed funds that our listeners would likely be quick to avoid, Vanguard’s very own dividend growth fund (VDIGX) is one of the 17 funds measured that underperformed during this time frame.

Specifically, if you invested $100,000 into the Vanguard Dividend Growth fund on January 1st, 1995, and reinvested all of your dividends along the way, your investment would be worth just over $1.3M today. If, instead you invested the $100k in Vanguard’s S&P 500 fund, your investment would be worth just over $1.9M today, roughly a $600,000 difference.

What’s interesting – yet not all that surprising about these results – is that the % of dividend funds that underperformed since 1995 is right in line with all of the other studies that have been done comparing active investment management to passive indexing. Depending on what study you look at, what asset class is being examined, and what time frame is being measured, the underperformance of actively managed equity funds over longer time periods is right around 80-90%.

In other words, on average, 80-90% of actively managed funds have underperformed broad-based indexes like the S&P 500. And that’s exactly what we see when looking at the historical performance of dividend-focused funds.

Now, while 30 years is a decent time frame to measure, I will always take more history and more data if it’s available.

Again, because there aren’t many dividend-focused funds with long track records that are still in existence today, evaluating a time period beyond 30 years means we have to resort to uninvestable indexes.

In other words, you could not have invested directly in these indexes, but they do illustrate how a particular asset class – or a particular basket of stocks – would have performed during the time period being measured. And this is not unique to dividend strategies – more often than not, when I reference the long-term historical performance of an asset class going back 90+ years, I’m referencing uninvestable indexes, not actual funds you can invest in. It’s all we have to work with in many situations if we want to measure longer time periods and study market history.

So, with that in mind, if you attempt to look up the long-term performance of dividend strategies on your own by searching something like “dividend stock performance” in Google images, you’ll be greeted with countless historical charts showing that “dividend-paying stocks” have dramatically outperformed non-dividend-paying stocks since 1927.

These charts and images measure the performance of custom-created indexes, and while they are technically accurate based on what is being measured, they are often the cause of many misunderstandings and misconceptions about dividend investing.

The conclusion that (I think) many people come to when they see these charts is, if dividend-paying stocks significantly outperform non-dividend-paying stocks over long periods of time, then dividend investing and buying high-yielding dividend stocks must be a superior investment strategy.

But that’s not really the case, these charts don’t tell the full story for a few reasons.

First, for most of the 1900s, dividends contributed to a much larger percentage of the overall market returns than they do today. For example, from 1871 to 1960, the dividend yield of the S&P 500 never fell below 3%. In addition, from 1970 to 1990, the dividend yield for U.S. stocks was 4%.

For comparison, today, the S&P 500 dividend yield is hovering around 1.35%. So, why is this important? Well, if an analysis of an index comprised of dividend paying stocks includes these decades where dividends were a bigger driver of total returns in the market, then the outcome will certainly favor stocks that pay dividends compared to stocks that don’t pay them.

Second, as noted in part one, roughly 75% of U.S. stocks pay a regular dividend. With that in mind, it shouldn’t be surprising that if you remove 75% of stocks from the U.S. stock market, returns will be significantly lower. Dividend stocks or not, if you don’t give me any other information, and just ask me to choose between investing in 75% of all U.S. companies or just 25% of them, I’m going to opt for the 75% basket every time.

Without any additional information, I’d prefer to own as much of any market as possible. This is the general definition (or philosophy) of passive index investing – instead of trying to pick the good stocks and eliminate all of the bad ones, just buy the entire market through a broad-based passive index fund.

If you only invest in 25% of the stock market and eliminate the other 75%, you’re making a very active investing decision. And, as I just highlighted, most active investing strategies, over long periods of time, underperform passive strategies by a wide margin.

So, yes, according to many of these charts, dividend-paying stocks – which represent about 75% of the broad U.S. market – outperformed non-dividend stocks, the other 25%, over the last 90+ years. At a high level, that shouldn’t be very surprising.

But taking it a step further, the better explanation for the outperformance shown in many of these charts is the fact that dividend investing is rooted in value investing, i.e., buying companies at low relative prices and holding them for long periods of time.

Since boring, unloved value stocks do often pay dividends – and academic research shows that value investing improves the expected return of a portfolio – it shouldn’t be a surprise that a giant basket of stocks with some value characteristics that happen to pay regular dividends outperforms a basket of expensive, non-dividend paying stocks.

As Meb Faber wisely put it in one of his many papers on this topic, “If you are adamant about buying dividend stocks, you MUST include a valuation screen to avoid the expensive, junky ones.” In other words, it’s not prudent to solely rely on the dividend yield of a stock or fund as a guide to constructing your portfolio.

If you must buy dividend stocks because you are passionate about dividend investing and believe it’s the right strategy, you should also measure the relative value of the stocks or funds you’re considering to avoid buying overpriced companies with lower future expected returns.

I touched on this briefly in last week’s episode when I mentioned that Warren Buffet would prefer to buy a cheap, low-dividend-yielding stock than an expensive, high-yielding one. This is another way of saying that the dividend yield should be irrelevant to the investment decision.

What matters most is that we are buying good companies (or good asset classes) at a good price. The company I buy at a low price – or index fund I buy at a low price – might pay regular dividends, but the fact that the company (or the fund) pays a dividend, won’t influence my investing decision.

As shared last week,

“Valuation matters. The price which you pay for an asset has a significant influence on the return (or lack thereof) that you’ll get.”

So, to recap where we’re at:

– Dividend investing is rooted in value investing.

– Value investing, implemented correctly, has historically provided investors with higher long-term returns. This is not because of the dividend yield but because value investors—or value funds—are buying good companies at low relative prices and patiently holding them for a long period of time. Many of those good companies just so happen to pay a dividend.

– Finally, if you evaluate a large basket of stocks that includes a healthy percentage of companies with value characteristics, it shouldn’t be surprising that it outperforms a basket of overpriced, overvalued stocks.

So, back to these dividend charts that you’ll find all over the internet. Why are these charts touting the outperformance of dividend stocks misleading or incomplete? Well, two reasons.

1) Because a high dividend yield is not the reason that an index comprised of dividend-paying stocks outperforms. It’s the fact that the stocks being measured have value stock characteristics.

2) If the goal is to show a superior investment approach by showing the long-term historical performance of different asset classes, the chart creators should also include properly constructed value strategies. If they did, as some academics have done, a dividend portfolio focused on yield wouldn’t look as appealing.

If an investor wants to improve the expected returns of a portfolio, they should really just hunt for value, not dividend yield. As Meb Faber and many others have shown through their research, doing this results in superior historical performance. In short, what they found is the more concentration a portfolio has in value stocks, the higher the returns have been.

Said another way, a properly constructed value portfolio has outperformed portfolios that are focused purely on the highest dividend yield over long periods of time. The value portfolio will likely pay regular dividends, but the dividend yield did not influence the construction of the portfolio.

Really quick, before we move on, it’s worth noting that value investing, even if the research supports it, is not a no-brainer or a one-size-fits-all solution.

As I’ve said countless times on this podcast, “The best investment strategy is the one you can stick with.” And, value investing can often be a hard strategy to stick with, especially if you don’t understand it. Like any investment strategy, value investing can go in and out of favor, sometimes for long periods of time.

If your value portfolio underperforms the broad markets for, let’s say, 10 years, would you be able to stick with it? If you can’t, then you might consider a different approach, even if all the evidence says that the other approach you’re considering is likely to produce lower returns. As the old adage says, time in the market is more important than timing the market.

You’re likely to have a better investment outcome over a long period of time if you stick with your chosen investment strategy – the one you know and understand and meets your unique goals – and avoid chasing trends or tricking yourself into believing the grass is greener somewhere else every few years.

Ok, as promised, to tie a bow on today’s episode, I want to highlight and summarize the three primary reasons why dividend-focused strategies typically underperform. Push historical performance to the side.

Without knowing what the historical performance has been, these reasons on their own should reinforce why dividend investing isn’t the magical solution it’s often marketed as, and why investors should expect the majority of dividend-focused funds to underperform over long periods of time going forward.

- Reason #1 – Dividend-focused strategies are often poorly constructed. We’ve already touched on this, but to briefly recap, the highest-yielding dividend stocks have the highest yields for a reason – they typically have high yields because they are junky, overpriced companies trying to attract more investors. If you buy a basket of high-yielding stocks – or buy a high-yielding mutual fund or ETF – it will naturally include some of these junky, overpriced companies which are likely to drag down the long-term returns of the portfolio.

Once again, if you must choose stocks or funds based on the dividend yield, you should also apply a valuation screen so you avoid these overpriced companies with lower expected future returns.

- Fees. Dividend-focused mutual funds and ETFs – even those offered by low-cost providers like Vanguard – have higher expense ratios than simple, broad-based index funds. For example, the Vanguard Total Stock Market Fund has an expense ratio of 0.04%.

On the other hand, the Vanguard Dividend Growth Fund has an expense ratio of 0.30%, a 25 basis point difference. Even worse, actively managed dividend funds like the Columbia Dividend Opportunity fund have expense ratios of 1% or more. According to Vanguard themselves, internal fund fees reduce investors’ returns.

In fact, Vanguard has gone as far as saying that the expense ratio of an investment is the best predictor of future returns. That lower-cost funds are more likely to outperform higher-cost funds. So, if dividend-focused funds – especially poorly constructed dividend funds – continue to charge higher fees, those fees will continue to put downward pressure on future returns.

- Lastly, number three, is taxes. And this is the one area we haven’t touched on yet, which we will get into more in a future episode of this series. But, in short, when you invest in dividend-focused stocks or funds in a taxable brokerage account, you are taxed every time you receive a dividend.

Even if you reinvest the dividend and don’t spend it, you’re taxed in the year it’s issued. All of the historical performance charts and articles touting the outperformance of dividend investing do not take taxes into consideration. The returns are quoted before fees and before taxes. And, depending on your tax bracket, research has shown that the tax effect on dividends can reduce your annual returns by up to 1.5% per year. If an investor is faced with two investment options with the same risk/return profiles, the investor is likely wise to choose the one that is more tax efficient.

And, yes, a tax-efficient investment is not immune to taxes like capital gains, but the investor has more control over when those taxes are paid versus receiving a regular taxable dividend every single quarter that they don’t really need or want. Also, in many cases, long-term capital gains are more favorable to the investor than taxes on dividend income.

So, the three primary reasons dividend-focused investments have underperformed are poor construction, higher-than-average fees, and taxes. Dividend investing or not, if an investment strategy contains expensive, overpriced companies, high internal fees, and poor tax efficiency, odds are that it will underperform over long periods of time. Those are a lot of hurdles to overcome.

If an investment fund is holding itself out as a dividend-focused fund, and it has produced sizeable outperformance, it’s either because the fund properly screened for value and avoided high yielding, overpriced stocks or the fund manager just got lucky. And, while luck can and often does play a role in investing, I’d like to believe that the long-term outperformance of a dividend strategy was really just due to it being a well-constructed value fund disguised and marketed as a dividend fund.

Which is not necessarily uncommon. After all, these fund companies can only be successful if investors allocate money to them, and a “tactical rising dividend income fund” is certainly more appealing than a “U.S. value fund.”

While I did highlight many of the issues with dividend investing today, I hope it’s clear that dividends are not inherently bad. Conversely, they also aren’t the key to unlocking higher-than-average investment returns. Good companies or good funds might pay dividends, but it’s not the dividends that make them good investments.

If you want to explore the research further, I’ll link to several studies and articles in today’s show notes, which can again be found at youstaywealthy.com/218.

Thank you, as always, for listening. I look forward to seeing you back here for part 3 of this series next week.

Disclaimer

This podcast is for informational and entertainment purposes only and should not be relied upon as a basis for investment decisions. This podcast is not engaged in rendering legal, financial, or other professional services.